Pet Insurance Distribution Channels: Top 5 Dominating U.S. Sales (2026)

By Hitul Mistry, Founder of Insurnest, who brings a decade of experience building technology for the insurance industry across India, the UAE, and the US.

Introduction

The U.S. pet insurance market crossed $5.2 billion in written premium, a 20.8% increase over the prior period. North America now has 7.03 million insured pets. And yet, the U.S. pet insurance penetration rate sits at just 5.46% for dogs and 2.04% for cats.

Read those numbers together and the strategic picture comes into focus. The pet insurance market size is large. The growth is fast. And the white space is far larger than the market itself, with more than 94% of American dogs and nearly 98% of cats remaining uninsured.

For carriers, MGAs, and agencies trying to capture that white space, the most important strategic question is not what to sell. The products are mature, the coverage structures are well understood, and the underwriting models are converging. The question that actually separates winners from also-rans is where to sell it.

Distribution is the battleground. Knowing how to sell pet insurance profitably in the U.S. comes down to the channel mix, and today, five pet insurance distribution channels are doing the heavy lifting. Each reaches a different pet owner, at a different moment, with a different economic profile. Understanding how each one works, and where it fits in your pet insurance MGA distribution strategy for the first year, is the difference between scaling profitably and burning capital on acquisition.

Here is a detailed breakdown of all five pet insurance distribution channels, what each one is, how it performs, and how to choose between them.

At Insurnest, we build distribution and underwriting technology for pet insurance MGAs, carriers, and agencies, which means we spend our days inside the exact channel-economics decisions this article maps. The patterns below reflect what consistently separates profitable distribution from expensive guesswork.

1. What Is Direct-to-Consumer Pet Insurance Distribution, and Should Carriers or MGAs Use It?

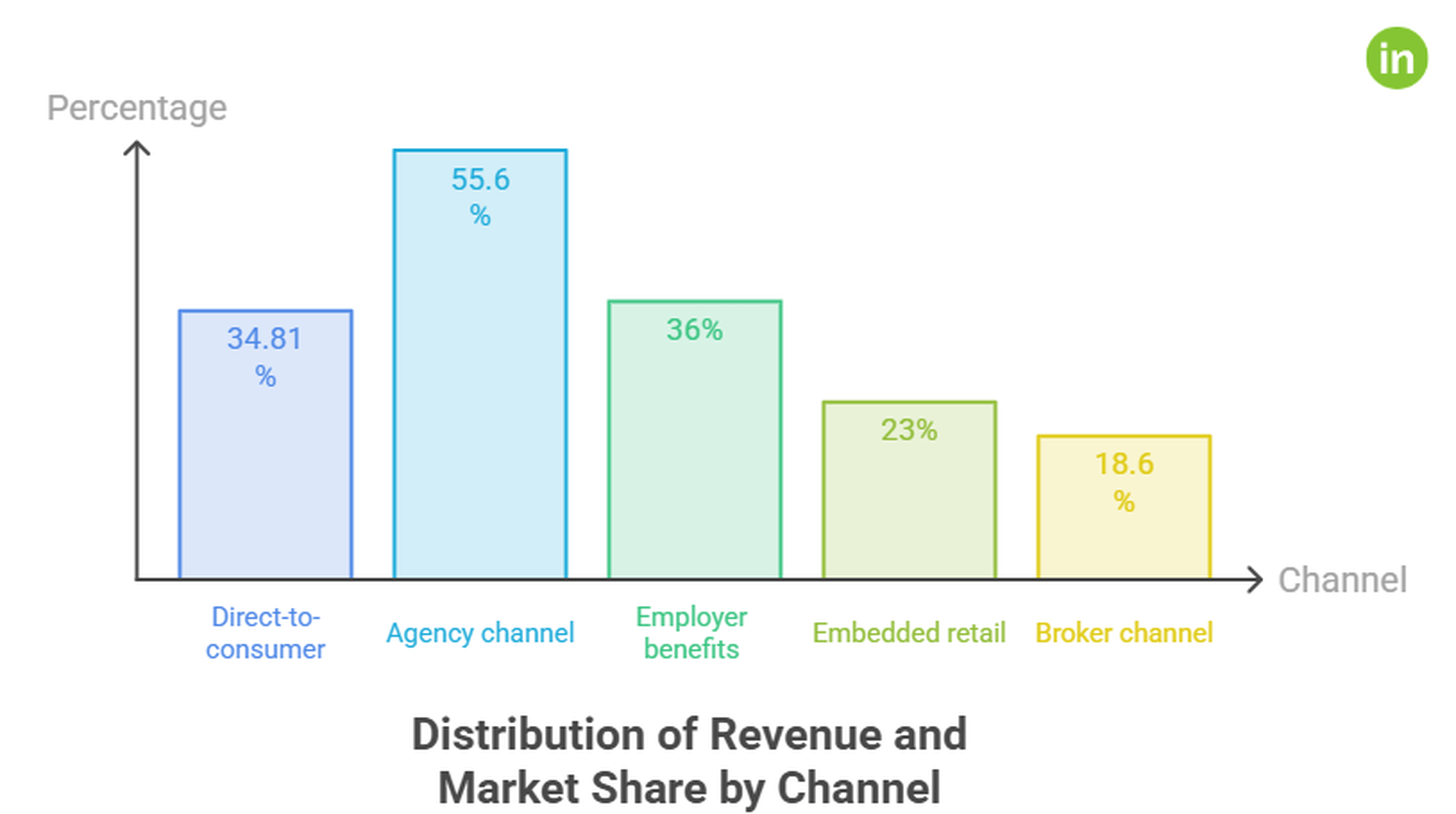

Direct-to-consumer (D2C) is when pet owners buy a policy straight from a carrier or MGA website, with no agent or broker in between. It is the largest single revenue channel in U.S. pet insurance at a 34.81% share (Grand View Research), and it best suits digital-first carriers and MGAs that want to own the customer relationship, the first-party data, and the brand.

How Does the Direct-to-Consumer Pet Insurance Channel Work?

The pet owner runs a quote, customizes coverage, and binds a policy entirely online on a carrier or MGA site, with no agent, broker, or referral involved.

The pet owner lands on a carrier or MGA website, runs a quote, customizes their deductible and reimbursement settings, and binds the policy online. No broker. No referral. No waiting-room conversation. The entire journey, from awareness to bound policy, happens inside a digital funnel the carrier controls end to end.

This is the channel most people picture when they imagine "modern" pet insurance: a slick mobile quote flow, instant pricing, and a policy issued in minutes. For a deeper look at how to build these direct-to-consumer digital channels for pet insurance MGAs, including funnel architecture and tech requirements, see our dedicated guide.

How Big Is the Direct-to-Consumer Pet Insurance Channel in the U.S.?

Direct sales lead the U.S. pet insurance market as the single largest revenue channel, and a wave of digital-first insurtechs built their entire presence on it.

According to Grand View Research, the direct segment led the U.S. pet insurance market with the largest revenue share of 34.81%. That dominance is driven by pet owners' preference to purchase policies directly from insurers for three reasons: convenience, faster policy issuance, and customized plan options.

A wave of digital-first insurtechs has built its entire market presence through direct-to-consumer distribution. These players didn't inherit an agent force or a legacy book. They competed on brand, user experience, and speed, and won roughly a third of the market doing it.

What Are the Pros and Cons of Direct-to-Consumer Distribution for Carriers and MGAs?

D2C gives you full ownership of the customer, data, and brand with no commissions, but customer acquisition cost is high, and conversion depends heavily on brand trust and mobile UX.

The defining advantage of D2C is ownership. You own the customer relationship, the renewal conversation, the cross-sell opportunity, and, critically, the first-party data. In a market where customer lifetime value is everything, owning the policyholder directly means you control retention and upsell rather than renting access through an intermediary who takes a cut and a piece of the relationship.

There is no revenue share and no broker commission, which keeps your unit margin intact on every policy. And done well, D2C is the fastest path to building a recognizable consumer brand, the kind of brand recognition that eventually lowers your acquisition cost as people start searching for you by name.

But the trade-offs are real and they are expensive. Customer acquisition cost is high because you are buying every click, every quote, and every conversion through paid search, paid social, and content. Optimizing these direct-to-consumer online sales funnels is critical to making the economics work. Conversion depends heavily on mobile UX and brand trust, and a clunky quote flow or a name nobody recognizes will bleed conversions at every step. Newer entrants have to earn that trust from scratch, competing for attention against incumbents with far deeper marketing budgets.

Which Carriers and MGAs Should Use the Direct-to-Consumer Channel?

Digital-first carriers, insurtechs, and MGAs that want to own the policyholder relationship and have the marketing capital to fund paid acquisition.

Digital-first carriers, insurtechs, and MGAs that want to own the policyholder relationship and build a long-term brand, and have the marketing capital and UX maturity to support a paid acquisition engine. Tools like a conversion funnel analytics AI agent can help these players measure and optimize each step of the D2C journey.

Building a direct-to-consumer pet insurance funnel from scratch?

Visit Insurnest to learn how we help MGAs launch and scale pet insurance programs.

2. How Does the Agency Channel Work for Selling Pet Insurance, and Why Does It Dominate the U.S. Market?

The agency channel sells pet insurance through licensed agents who educate and guide pet owners, and it is the single largest distribution channel in North America at 55.6% of market share (Market Data Forecast). It dominates because personal advice builds trust and produces higher-quality, longer-retained policies than direct-only channels.

How Does the Agency Channel Work in Pet Insurance?

Licensed agents across independent, captive, and digital agency networks educate pet owners and guide them to the right policy, building trust at the point of decision.

Licensed agents work directly with pet owners through independent agencies, captive networks, and digital agency platforms. The agent's job is to educate, reduce buyer confusion, and guide the pet owner to the right policy, building trust at the point of decision and driving policy quality that direct-only channels often struggle to match.

This is the traditional backbone of insurance distribution, and in pet insurance it remains the single largest channel.

What Share of the Pet Insurance Market Does the Agency Channel Hold?

The agency channel is the largest pet insurance distribution channel in North America by market share, and that dominance is concentrated in the U.S., which makes up the bulk of the region.

According to Market Data Forecast, the agency segment dominated the North American pet insurance market and held 55.6% of the market share. That dominance is driven by the traditional role of insurance agents in educating pet owners and walking them through policy selection.

And here's the detail that matters for a U.S.-focused strategy: the U.S. accounts for 70.5% of the North American market. That means agency-channel dominance is heavily weighted toward U.S. distribution activity specifically. This isn't a Canadian or cross-border artifact, it's a reflection of how American pet owners actually buy.

The major carriers reflect this. Several leading pet insurers rely heavily on the agency channel, distributing through large independent agent networks and operating behind well-known consumer insurance brands. Others run agency distribution alongside their own direct channel, hedging across both.

What Are the Pros and Cons of the Agency Channel for Carriers and MGAs?

It is the largest channel by volume with strong retention from personal advice, but commissions add cost and scaling requires recruitment, training, and compliance infrastructure.

The agency channel is the largest channel by market share, full stop. If you want to be where the volume already is, this is it.

The personalized advisory approach is a genuine retention driver. When an agent explains why a particular deductible or reimbursement level fits a specific pet owner's situation, that buyer understands what they purchased and is far less likely to lapse out of confusion or buyer's remorse. Agent relationships also create ongoing touchpoints, a reason to talk to the customer again at renewal, when adding a second pet, or when bundling with other coverage.

The costs are structural. Designing the right agent commission and incentive programs for pet insurance MGAs is critical because agency commissions add a layer of distribution cost on every policy. Agent education is inconsistent across a large network, which creates variability in how well your product is represented and sold. And scaling the channel requires real investment in recruitment, training, and compliance infrastructure. You can't just flip a switch and have a national agent force.

Which Carriers and MGAs Should Use the Agency Channel?

Carriers and MGAs that already have agent networks, commission structures, and training programs, or the appetite and capital to build them.

Carriers and MGAs with established agent networks, commission structures, and training programs already in place, or the appetite and capital to build them. When operating across multiple channels simultaneously, a clear approach to channel conflict resolution in multi-channel pet insurance distribution becomes essential.

From the field: the carriers we see retain best through agents aren't the ones paying the highest commission. They're the ones investing most in agent education, because a well-briefed agent sells the right policy the first time.

3. Can Carriers and MGAs Sell Pet Insurance Through Employer Benefits, and Is the Channel Worth It?

Yes. Pet insurance can be sold as a payroll-deducted voluntary benefit through employers and benefits brokers, and 36% of large U.S. employers now offer it (Mercer). It is worth it for players built for the channel: it delivers low acquisition cost and high retention, in exchange for long B2B sales cycles and benefits-platform integration.

How Is Pet Insurance Sold Through Employer Benefits?

It is offered to employees as a payroll-deducted voluntary benefit, sold into the employer through benefits brokers and HR, so one relationship reaches an entire workforce.

Pet insurance is offered to employees as a voluntary benefit, typically through payroll deduction, and sold into the employer through benefits brokers and HR decision-makers. One employer relationship unlocks access to an entire workforce at once, and because the premium comes out of payroll, the buying friction for the employee is dramatically lower. For a detailed look at how to build and price this channel, see our guide on employer voluntary benefits as a pet insurance MGA channel.

How Fast Is Employer-Sponsored Pet Insurance Growing?

Employer-sponsored pet insurance is expanding quickly among large U.S. employers, with adoption climbing steadily over the past five years and major group carriers driving it.

Among U.S. companies with 500 or more employees, 36% now offer pet insurance as an employee benefit, a 22% increase over the past five years, according to research from consulting firm Mercer. That growth trajectory tells you this is a channel in expansion, not maturity.

Carrier activity backs this up. Established group and voluntary-benefits carriers have moved into employer-based pet insurance offered through payroll deduction, frequently partnering with specialist pet insurance providers to broaden the voluntary benefits portfolios they bring to employer clients.

There's also a powerful narrative driving adoption. A widely cited industry study found that only 52% of pet owners who faced an unexpected pet health expense were financially prepared for it, down from 82% in a prior study. That widening financial-vulnerability gap is exactly the story benefits brokers are using to convince employers that pet coverage is a meaningful, low-cost addition to their voluntary benefits lineup.

A handful of large group and voluntary-benefits carriers lead the workplace channel, offering pet coverage as a payroll-deducted voluntary benefit through employers.

What Are the Pros and Cons of the Employer Benefits Channel?

Payroll deduction delivers low acquisition cost and high retention, but sales cycles are long and the channel demands benefits-platform and payroll integration.

The economics of this channel are structurally attractive once you're in. A single employer relationship creates access to hundreds or thousands of potential policyholders without the per-customer acquisition cost of D2C. Payroll deduction produces meaningfully lower lapse rates, so the premium is automatic, and policies don't fall off because someone forgot to pay or reconsidered at renewal. And employer endorsement removes the trust barrier entirely; when coverage is offered through your own workplace benefits portal, it carries implicit credibility that a cold digital ad never will.

But getting in is hard and slow. Sales cycles run long, threading through benefits brokers and HR approval processes that move on annual enrollment calendars, not your growth timeline. Participation can stay low without active, well-designed employee communication: offering the benefit isn't the same as getting employees to elect it. And the channel demands heavy platform integration. You need to connect into benefits administration systems and payroll deduction infrastructure to operate at all. A group pet insurance benefit design AI agent can help MGAs structure competitive employer benefit packages and pricing models for this channel. For further reading on carrier backing and employer group pet insurance pricing, see our dedicated analysis.

Which Carriers and MGAs Should Use the Employer Benefits Channel?

Carriers and MGAs with group enrollment capability, payroll deduction infrastructure, and benefits broker relationships at scale.

Carriers and MGAs with group enrollment capabilities, payroll deduction infrastructure, and benefits broker relationships at scale, those equipped to play a longer B2B sales game in exchange for high-retention, low-CAC volume.

4. What Is Embedded Pet Insurance Distribution, and How Do MGAs Use It to Acquire Customers?

Embedded distribution places the pet insurance offer inside an experience the owner is already in, a retailer's checkout, an e-commerce flow, a vet visit, or an adoption, using API-based quoting. It now drives roughly 23% of pet insurance premiums (industry estimates), giving MGAs low-cost, high-relevance customer acquisition in exchange for revenue sharing and less direct ownership of the customer.

How Does Embedded Pet Insurance Distribution Work?

The insurance offer is built into a platform the pet owner is already using, checkout, e-commerce, a vet visit, or adoption, and bound in the moment via API-based quoting.

Embedded distribution puts the insurance offer in front of the pet owner at the exact moment they're already thinking about their animal, inside a retailer's checkout, an e-commerce flow, a vet clinic's payment process, or an adoption journey. Instead of paying to find pet owners, you partner with a platform where they already are and embed the coverage offer into an experience they're already engaged in. For a deep dive into embedded insurance API-based distribution for pet insurance MGAs, including technical architecture and partner integration patterns, see our implementation guide.

The best moment to offer pet insurance is when a pet owner is already focused on their pet. Embedded distribution engineers that moment at scale.

How Much of the Pet Insurance Market Is Embedded Distribution?

Embedded now accounts for a substantial, mainstream share of pet insurance premiums across North America and Europe, led by point-of-care and point-of-adoption models.

The marquee partnerships show how mainstream this has become. National pet retailers have launched co-branded pet insurance products integrated with their own in-store and mobile veterinary services. Major pet e-commerce platforms now offer insurance directly inside the buying experience, placed where pet owners already spend on food, medication, and supplies. And large commercial underwriters back affinity programs distributed direct, through affinity groups, and through employer-sponsored voluntary benefit programs. Understanding how to structure these embedded pet insurance partnerships for MGA revenue is key to making the economics work.

One market research report estimates that approximately 23% of pet insurance premiums across North America and Europe came through embedded channels. That's not a fringe experiment. Nearly a quarter of premium is flowing through embedded distribution. It is no longer a secondary strategy. It is a mainstream one.

The point-of-care and point-of-adoption models are especially powerful. Some carriers pioneered the embedded model at the point of care through direct-pay arrangements across more than 11,000 vet clinics. Tools like a vet partnership AI agent help MGAs manage and scale these veterinary distribution relationships. Others embed at the moment of adoption, reaching owners at the precise instant they bring a new shelter or rescue animal home. Our guide on animal shelter distribution for pet insurance MGAs covers how to approach shelters and rescues as distribution partners.

What Are the Pros and Cons of Embedded Pet Insurance Distribution?

Embedded delivers contextual timing and low media spend, but the partner usually owns the customer, revenue sharing compresses margin, and API-ready quoting is a hard prerequisite.

Embedded distribution's superpower is contextual timing. You reach the pet owner at their most receptive moment, buying supplies, visiting the vet, adopting a pet, when the relevance of coverage is self-evident and the decision feels natural rather than interrupted. The partner's existing trust transfers to your insurance offer, and your media spend is far lower than the brute-force paid acquisition that powers D2C.

The trade-offs sit on the other side of the ledger. The carrier rarely owns the customer relationship directly, the partner does, which complicates renewals, cross-sell, and data ownership. Revenue share with the platform compresses your margin on each policy. And there's a hard technical prerequisite: API-ready quoting. Without the ability to deliver real-time quotes and bind policies inside someone else's checkout flow, you simply can't play in this channel. Our guide on API integration for pet insurance MGA technology vendors explains how to evaluate and implement the technical stack, and an embedded API AI agent can manage the real-time distribution APIs across multiple partner platforms.

Which MGAs and Carriers Should Use Embedded Distribution?

Tech-ready MGAs and carriers with API-based quote flows, white-label journey capability, and partner reporting infrastructure.

Ready to launch API-first embedded pet insurance distribution?

Visit Insurnest to learn how we help MGAs launch and scale pet insurance programs.

Tech-ready MGAs and carriers with API-based quote flows, white-label journey capability, and partner reporting infrastructure, the players who can integrate cleanly into a partner's experience and report performance back to them. An embedded pet insurance product design AI agent can help configure white-label products tailored to each partner's audience.

5. How Does the Broker Channel Work for Pet Insurance, and Why Is It the Fastest-Growing?

The broker channel sells pet insurance through independent brokers and comparison platforms that let pet owners weigh multiple carriers side by side. It is the fastest-growing distribution channel in North America at an 18.6% CAGR (Market Data Forecast), delivering high-intent comparison shoppers, with price competition and limited brand control as the main trade-offs.

How Does the Broker Channel Work in Pet Insurance?

Independent brokers and comparison platforms let pet owners compare multiple carriers side by side, so buyers arrive high-intent and ready to choose.

Brokers operate independently of any single carrier, helping pet owners compare plans across multiple providers and choose based on unbiased advice. The buyer arrives already in shopping mode, comparing options, weighing coverage against price, which makes them high-intent and further down the purchase funnel than a cold prospect. A quote comparison AI agent automates the multi-carrier comparison process, making it easier for brokers and platforms to present side-by-side options at scale.

How Fast Is the Pet Insurance Broker Channel Growing?

The broker segment is the fastest-growing pet insurance distribution channel in North America, driven by demand for independent, multi-carrier comparisons.

According to Market Data Forecast, the broker segment is estimated to register a CAGR of 18.6%, the highest growth rate of any distribution channel in North America. That growth is driven by pet owners increasingly seeking independent advice and multi-carrier comparisons rather than buying blind from a single brand.

The comparison platforms demonstrate the scale this channel can reach. Leading multi-carrier comparison services are licensed across all 50 U.S. states and D.C. and have helped 2 million or more pet parents compare plans, with the largest vet-endorsed advisory platforms having served well over 1 million pet owners each.

And one carrier shows just how far the broker channel can be leaned on: at least one established pet insurer draws roughly 90% of its business through brokers. That's a near-total commitment to independent distribution, and it works.

What Are the Pros and Cons of the Broker Channel for Carriers and MGAs?

It is the fastest-growing channel and reaches high-intent buyers, but brand control is limited and price tends to become the main differentiator.

The broker channel is the fastest-growing channel by CAGR, which makes it strategically important for anyone planning where the market is heading rather than where it has been. Broker independence means buyers get genuine multi-carrier comparisons, and the buyers who reach a broker are high-intent: they've already decided they want coverage and are choosing between options, not deciding whether to buy at all.

The costs come down to control and competition. You have limited brand control when your product sits on a comparison page alongside every competitor. In that context, brand loyalty in pet insurance becomes an opportunity rather than a threat for MGAs that invest in differentiation beyond price. Price tends to become the primary differentiator, which can pressure margins and commoditize your offer. And building broker relationships adds operational overhead, including appointments, integrations, and ongoing management.

Which Carriers and MGAs Should Use the Broker Channel?

Carriers and MGAs seeking fast distribution reach and high-intent comparison shoppers, especially when entering new markets without brand recognition.

Carriers and MGAs seeking faster distribution reach and access to high-intent comparison shoppers, particularly useful when entering new markets where you don't yet have brand recognition or an agent force.

Which Pet Insurance Distribution Channel Should MGAs and Carriers Prioritize First?

There is no single best channel. Start where your strengths lie: direct-to-consumer for digital-first MGAs, the agency channel for established carriers, embedded for tech-ready MGAs, and the agency channel for anyone focused on long-term retention. The winners build across all five channels over time.

There is no universally correct starting channel. The right pet insurance distribution strategy depends on your business model, your existing infrastructure, and your strategic goals, and pet insurance MGA distribution looks very different from an established carrier's. A digital-first insurtech and an established multi-line carrier should not start in the same place, and neither should treat any single channel as the whole answer. Building a detailed distribution ramp plan for your pet insurance MGA is the first step toward getting the sequencing right.

Here's a practical decision guide for choosing among the pet insurance sales channels, based on where you're starting from:

| Your Situation | Start Here | Build Toward |

|---|---|---|

| Digital-first MGA entering the U.S. market | Direct-to-consumer | Broker channel for volume while SEO and brand develop |

| Established carrier with agent networks | Agency channel | Employer benefits + Embedded to extend reach |

| Tech-ready MGA with API infrastructure | Embedded retail and affinity | Broker channel for high-intent buyers + Direct for retention |

| Carrier building brand awareness from scratch | Broker channel and agency networks | Employer benefits for policy quality and volume |

| Any carrier focused on long-term retention | Agency channel | Direct-to-consumer for renewal ownership and upsell |

The pattern across every row is the same: start where your existing strengths let you win quickly, then expand into the channels that round out your reach and lock in retention. The starting channel buys you early traction. The "build toward" channel is where durable advantage compounds. Using a channel performance analytics AI agent across all active channels helps you measure cost-per-acquisition, conversion, and retention by channel, so you know where to double down and where to cut spend.

For MGAs running multiple channels, understanding your pet insurance channel partnerships holistically, and measuring MGA retention rates across a multi-line portfolio, is what separates data-driven scaling from guesswork.

Not sure which pet insurance distribution channel to build first?

Visit Insurnest to learn how we help MGAs launch and scale pet insurance programs.

What Is the Bottom Line on Pet Insurance Distribution Strategy in the U.S.?

The bottom line: U.S. pet insurance growth is a distribution problem, not a product problem, and the carriers and MGAs that win will build across all five channels rather than betting on one. With dog penetration at just 5.46% and cat penetration at 2.04%, the opportunity goes to whoever can reach the most underserved pet owners.

The U.S. pet insurance market is large, growing, and underpenetrated. With dog penetration at 5.46% and cat penetration at 2.04%, the overwhelming majority of American pet owners remain uninsured. That is not a product problem. It is a distribution problem. A market penetration analytics AI agent can model exactly where penetration gaps are widest and which channels are best positioned to close them.

The numbers map the opportunity precisely:

- The agency channel holds 55.6% of the North American market.

- The broker channel is growing at 18.6% CAGR, the fastest of any channel.

- Direct-to-consumer owns 34.81% of U.S. revenue.

- Embedded retail accounts for roughly 23% of premiums.

- Employer benefits are now offered by 36% of large U.S. employers.

Every channel plays a different role. Each reaches a different pet owner, at a different moment, with a different cost structure and a different retention profile. And none of them closes the penetration gap alone.

The carriers and MGAs that win the next phase of this market will not bet everything on one channel. They will build across all five, measure the economics of each with discipline, and scale aggressively where the returns are strongest, while pruning where they aren't.

Breadth across all five pet insurance distribution channels is the competitive advantage. The white space is enormous, the growth is real, and the window to build the infrastructure to capture it is open now.

Ready to build your multi-channel pet insurance distribution engine?

Visit Insurnest to learn how we help MGAs launch and scale pet insurance programs.

Frequently Asked Questions

What are the main pet insurance distribution channels in the U.S.?

The five dominant channels are direct-to-consumer, the agency channel, employer voluntary benefits, embedded retail and affinity partnerships, and the broker channel. Each one operates with a distinct cost structure, conversion funnel, and retention profile, so the right mix depends on your infrastructure and growth goals.

Which pet insurance distribution channel has the largest market share?

The agency channel is the largest, holding 55.6% of the North American market (per Market Data Forecast). Agents educate pet owners at the point of decision, which builds trust and produces higher-quality, longer-retained policies than channels that rely purely on self-service.

Which pet insurance distribution channel is growing the fastest?

The broker channel is the fastest-growing at an 18.6% CAGR (per Market Data Forecast). Pet owners increasingly want independent, multi-carrier comparisons before committing, and comparison platforms are making that easy at national scale.

What is embedded pet insurance distribution?

Embedded distribution integrates the insurance offer into a platform the pet owner is already using, such as a retailer's checkout, an e-commerce site, a vet visit, or an adoption journey. API-based quoting delivers real-time pricing, and this channel now accounts for roughly 23% of premiums (industry estimates).

How does the direct-to-consumer pet insurance channel work?

Pet owners visit a carrier or MGA website, run a quote, customize coverage, and bind a policy entirely online with no agent or broker. It is the largest single revenue channel in U.S. pet insurance at a 34.81% share (per Grand View Research), favoring digital-first players with strong UX and brand.

How does the employer benefits channel work for pet insurance?

Pet insurance is offered as a payroll-deducted voluntary benefit through employers, sold in via benefits brokers and HR teams. With 36% of large U.S. employers now offering it (per Mercer), the channel delivers low acquisition cost and strong retention through automatic payroll deduction.

Which pet insurance distribution channel should an MGA or carrier prioritize first?

Start where your strengths are strongest: direct-to-consumer for digital-first MGAs, the agency channel for carriers with existing agent networks, embedded for API-ready MGAs. The winners expand into all five channels over time, measuring economics rigorously at each stage.

Why is U.S. pet insurance growth considered a distribution problem?

With dog penetration at just 5.46% and cat penetration at 2.04% (per NAPHIA), over 94% of American dogs and 98% of cats are uninsured. The products are mature and well-understood. Growth now hinges on reaching those underserved owners through the right combination of distribution channels.

A Note on the Data

The figures in this article are drawn from published industry research, including NAPHIA's State of the Industry data, Grand View Research, Market Data Forecast, Mercer, and the MetLife pet health spending study. Market-share and growth figures reflect each source's most recent reporting period, and some use different geographic scopes (U.S. versus North America). We've noted this inline where it affects interpretation. Where sources report different headline market-size figures, we've used the most recent NAPHIA-aligned estimate. All sources are listed below.

Sources

- NAPHIA State of the Industry

- Grand View Research — U.S. Pet Insurance Market Report

- Market Data Forecast — North America Pet Insurance Market

- Mercer — via HR Dive

- MetLife Pet Health Spending Study

- SkyQuest — Pet Insurance Market Report

About the Author

Hitul Mistry is an InsurTech leader with more than a decade of experience in insurance and technology. He enjoys solving various business problems with the help of Technology. He has experience working with Brokers, Insurance Carriers, Reinsurance firms. He has experience working in India, the UAE and the US markets.

Disclosure: Insurnest builds distribution technology for pet insurance MGAs and carriers. This article is educational and reflects our independent analysis of publicly reported industry data.