Pet Insurance Penetration Rate Below 4%: What MGAs Must Do to Close the Gap

What Is the Current State of Pet Insurance Penetration in the US?

Pet insurance has quietly emerged as one of the fastest-growing segments in insurance. The forces behind it are structural and durable: rising pet ownership, increasing veterinary expenses, and a fundamental shift in how people regard their animals. Pets are now considered family members, and owners are spending more than ever on their wellbeing. Add in the rise of digital insurance adoption and a younger generation of buyers, Millennials and Gen Z, and the demand outlook is strong.

North America leads this expansion, with 7M+ insured pets and a written premium market north of $5B. Yet the US remains notably underpenetrated. The US pet insurance penetration rate reached just 3.92% in 2024, still below 4%. Dogs are covered at a higher rate than cats, at roughly 5.46% versus 2.04%.

That leaves a substantial uninsured market. Most pets still have no policy at all, which presents a significant growth opportunity for insurance carriers, MGAs, brokers, embedded insurance platforms, and vet-tech companies alike.

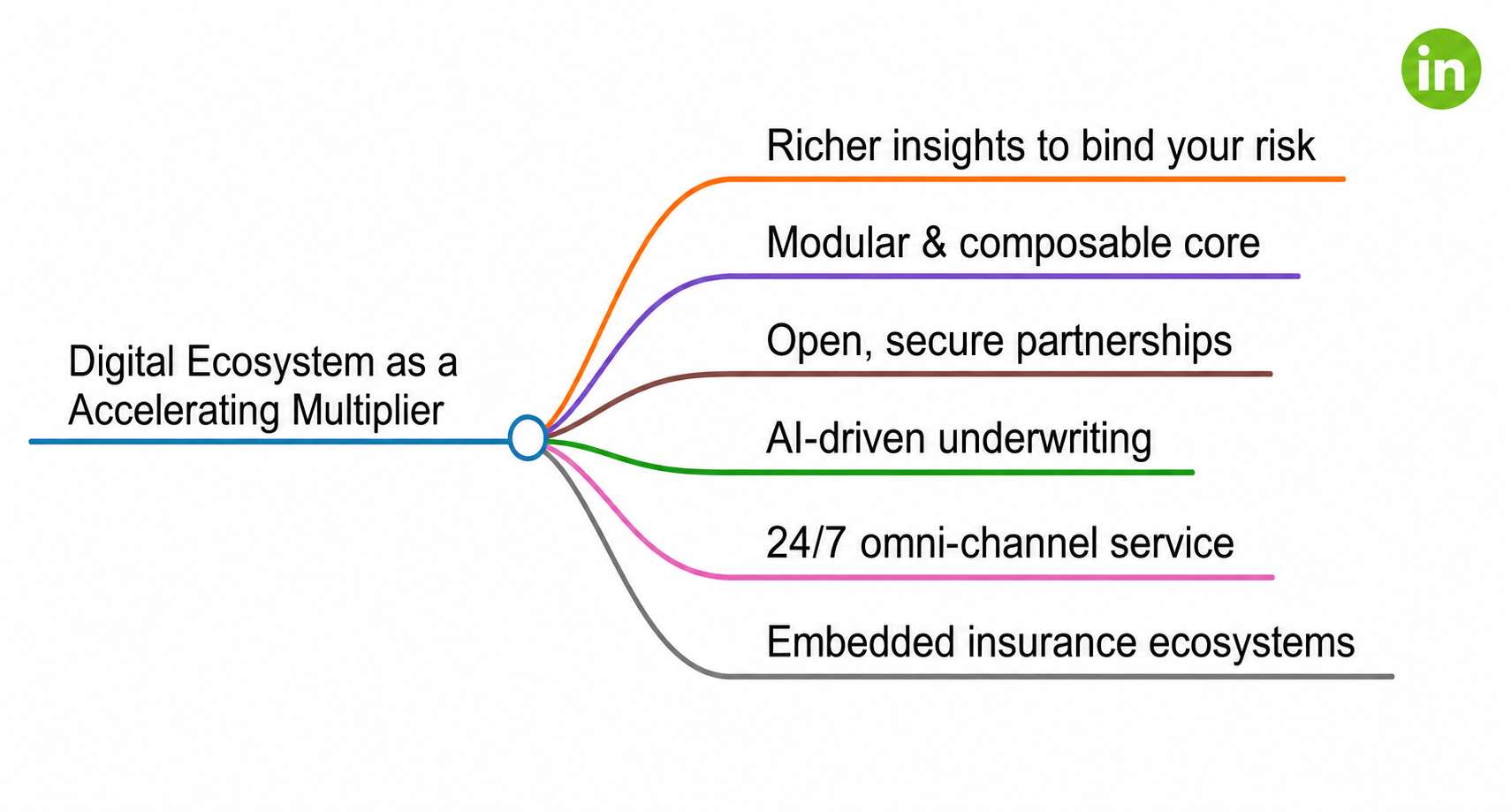

Digital ecosystems are driving penetration forward. Technology is doing much of the work in bridging this gap:

- Digital quote-to-bind journeys lower onboarding friction, streamline the purchase process, and lift conversion rates.

- Mobile-first experiences align with how younger customers prefer to buy, improving accessibility and convenience.

- Faster claims processing through OCR-based automation and vet invoice digitisation reduces reimbursement delays and strengthens customer trust.

- AI-driven underwriting accelerates policy issuance and enables personalised pricing, enhancing the overall experience.

- Self-service portals make policy management and real-time claim tracking straightforward, improving transparency.

- Embedded insurance ecosystems place coverage in front of buyers during pet adoption, vet visits, and pet product purchases, widening accessibility and helping penetration advance faster.

Underlying all of this is a shift in customer expectations. Buyers now want faster onboarding, straightforward policy comparison, transparent pricing, real-time claim tracking, quicker reimbursement, and a subscription-style experience.

What Are the Core Questions Defining the Next Phase of Pet Insurance Penetration?

The core questions defining the next phase of pet insurance are how to increase penetration faster, how to build trust, how to simplify buying and claims, and how to make coverage more affordable. These are the four challenges the industry must solve to move from a 3.92% penetration rate toward mass-market adoption.

The demand clearly exists. The problem is that adoption is still slower than the market's potential. Which raises the questions that define the next phase of this industry:

- How can insurers increase penetration faster?

- How can they improve trust?

- How can they simplify buying and claims?

- How can they make pet insurance more affordable?

Why Is Pet Insurance Penetration Still Low? Because Most Pets Remain Uninsured

Pet insurance penetration stays low because more than 96% of US pets are still uninsured. Low awareness, affordability concerns, and limited visibility at the right purchase moment are the primary reasons adoption has not yet reached scale.

The headline number tells the story plainly: US overall pet insurance penetration reached 3.92% in 2024. Put differently, more than 96% of pets are still uninsured. The gap is uneven across pet types. Dog penetration sits higher at around 5.46%, while cat penetration trails at just 2.04% and that lower cat adoption pulls the overall average down. The key insight here is a subtle but important one: pet insurance adoption is genuinely growing, but it has not yet reached mass-market adoption. The category has momentum without scale, a growing market that remains, for now, the exception rather than the norm.

In the US pet insurance market, pet insurance penetration rate growth is no longer theoretical. The question is what is holding it back and how quickly those obstacles can be removed.

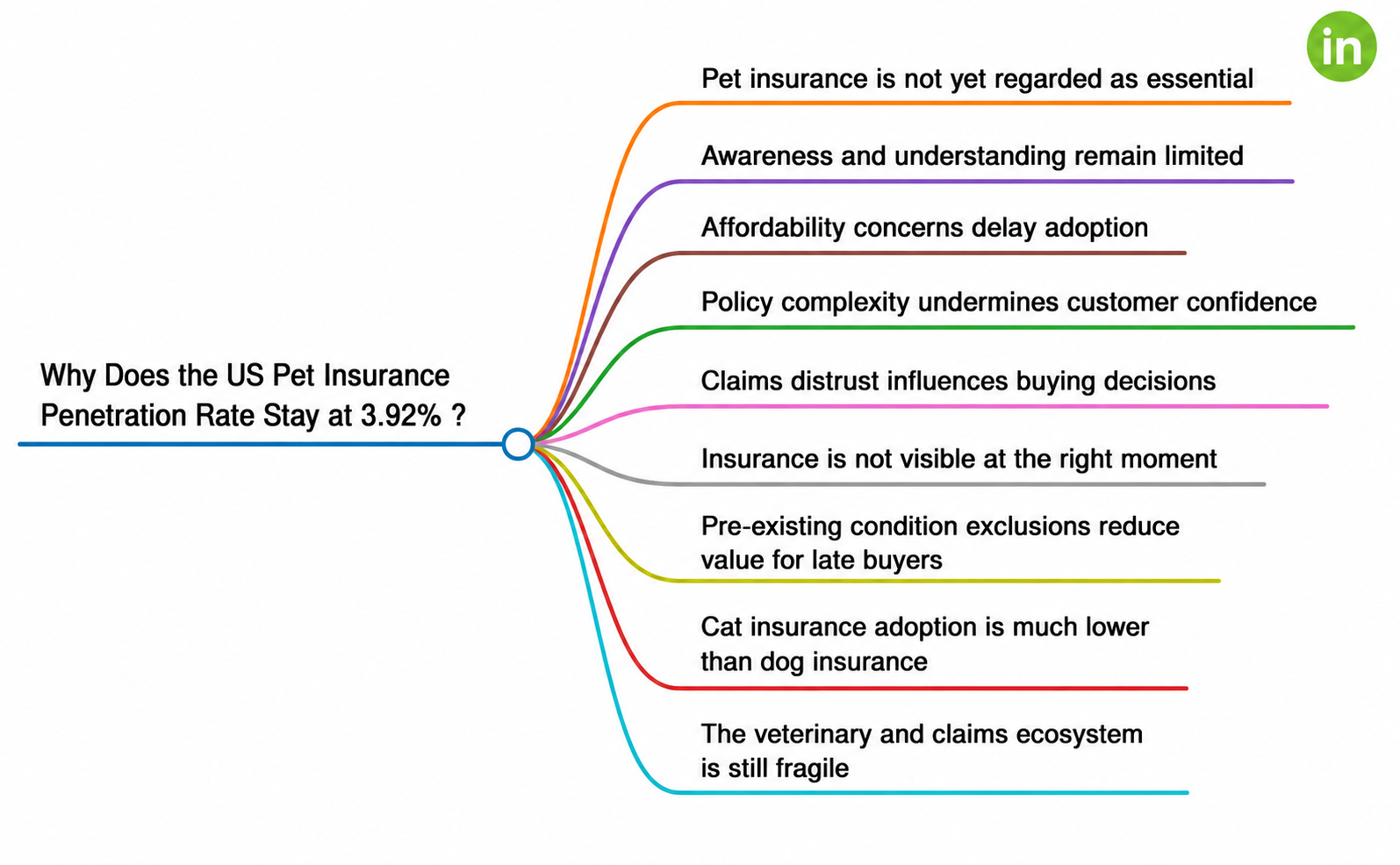

Why Does the US Pet Insurance Penetration Rate Stay at 3.92%?

If demand is rising, why does adoption remain stuck below 4%? The answer is not one single barrier. It is a series of frictions that accumulate at every stage of the buying journey.

1. Pet insurance is not yet regarded as essential

Many owners still treat it as discretionary spending, prioritising visible, immediate costs first: food, grooming, accessories, routine vet visits. Insurance is frequently considered only after a large veterinary bill has already arrived.

2. Awareness and understanding remain limited

A large share of owners still do not clearly understand how pet insurance operates, what is covered, what is excluded, how reimbursement works, or why early enrolment is important. That limited awareness directly suppresses early-stage adoption.

3. Affordability concerns delay adoption

Monthly premiums can feel like an additional expense, and multi-pet households face a heavier total burden. Cost-conscious customers hold off. Average accident-and-illness premiums in 2023 ran around $676 per year for dogs and $383 per year for cats.

4. Policy complexity undermines customer confidence

Terms are difficult to compare side by side. Deductibles, reimbursement percentages, annual limits, waiting periods, exclusions, and pre-existing condition rules all generate confusion, and confusion produces hesitation before purchase.

5. Claims distrust influences buying decisions

Customers worry about claim rejection, delayed reimbursement, undisclosed exclusions, and complicated documentation. Because pet insurance typically runs on a reimbursement model, the customer pays the vet first, then files a claim, then waits, many buyers feel uncertain about the genuine value before they ever sign up.

6. Insurance is not visible at the right moment

Many owners never encounter an insurance offer during the key stages of pet ownership: adoption, the first vet visit, a pet retail purchase, a wellness subscription, or employer benefit enrolment. Late discovery results in a missed adoption opportunity.

7. Pre-existing condition exclusions reduce value for late buyers

If a pet already has a diagnosed condition, coverage may be restricted. Late buyers often feel insurance is no longer beneficial after a diagnosis, which generates frustration and further suppresses adoption.

8. Cat insurance adoption is much lower than dog insurance

Cat penetration sits at only around 2.04%. Cat owners may perceive lower health risk or less urgency, and that lower adoption pulls down overall penetration.

9. The veterinary and claims ecosystem is still fragmente

There is limited real-time connectivity between insurers, veterinary clinics, and claims systems. Manual invoice handling delays reimbursement, and the absence of standardised veterinary data makes automation challenging, all of which weakens the claims experience and erodes trust and retention.

In short, the US pet insurance penetration rate stays at 3.92% because awareness is still limited, insurance is viewed as optional, cost and complexity produce hesitation, claims trust is not fully established, distribution is not embedded enough, and too many customers discover insurance too late.

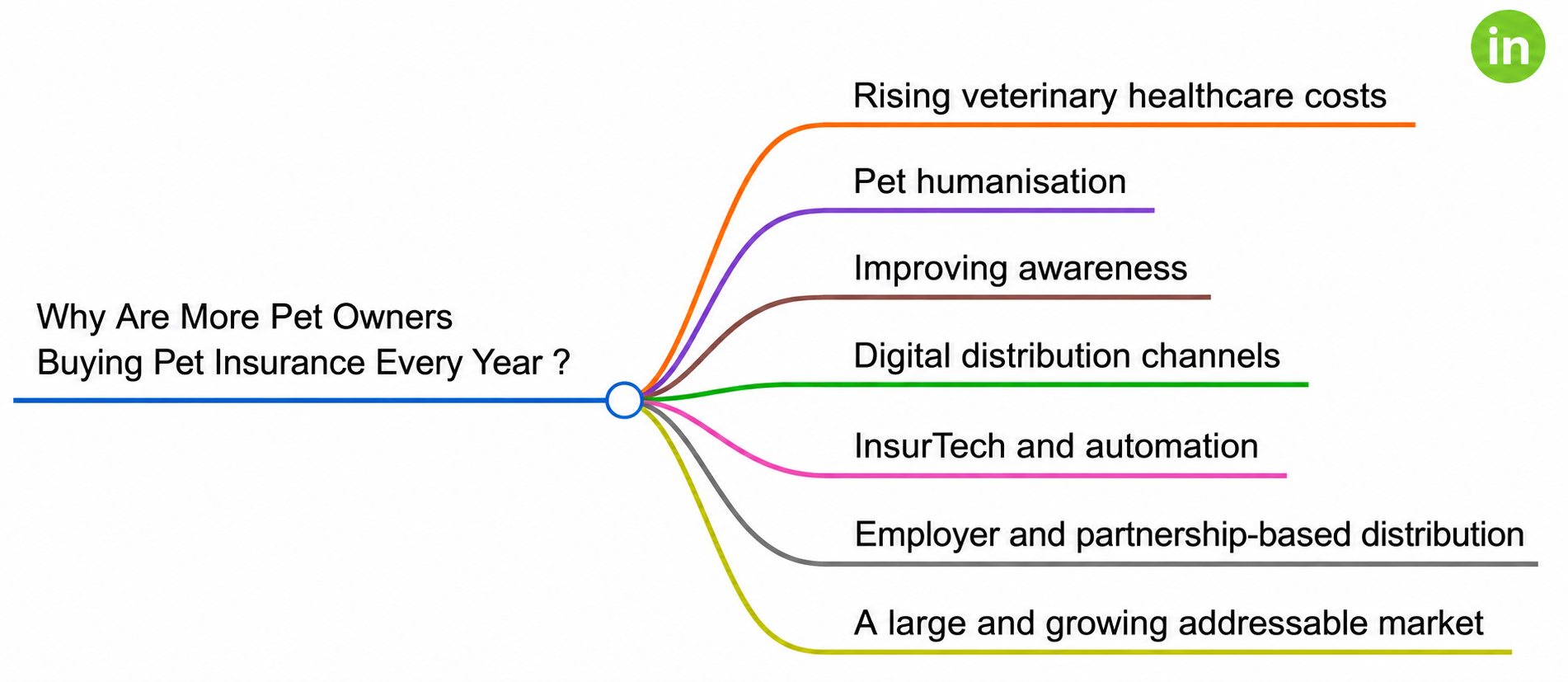

Why Are More Pet Owners Buying Pet Insurance Every Year?

If frictions are holding penetration back, what is pulling it forward? Several strong currents are moving more owners toward coverage every year.

1. Rising veterinary healthcare costs

Emergency treatments have become financially significant. Surgeries, chronic illness management, cancer care, and orthopaedic procedures can run into thousands of dollars. As a result, pet owners are increasingly seeking financial protection against unexpected expenses, and insurance is now viewed as a genuine healthcare support tool rather than a luxury.

2. Pet humanisation

Pets are increasingly regarded as family members, and owners are prepared to spend more on preventive care, wellness, long-term treatments, and premium healthcare services. That deepening emotional connection is directly increasing willingness to insure.

3. Improving awareness

Understanding of pet insurance is steadily growing. Social media is informing owners, veterinary clinics are raising insurance awareness, and influencer-driven pet content is increasing product visibility. There is simply more discussion now around reimbursement protection and treatment affordability.

4. Digital distribution channels

Accessibility is advancing through online quote-to-bind journeys that simplify onboarding and quicker policy comparisons that support purchase decisions. Embedded insurance models are broadening visibility, offered during pet adoption, through vet ecosystems, and through pet retailers and digital platforms.

5. InsurTech and automation

Technology is steadily elevating the customer experience: faster claims processing through OCR-based invoice handling, AI-assisted underwriting paired with real-time claim tracking, and reduced operational friction that builds customer confidence.

6. Employer and partnership-based distribution

Pet insurance is increasingly available as an employee benefit, and partnerships with veterinary hospitals, pet wellness platforms, retail ecosystems, and digital pet-care applications are widening insurance reach and customer accessibility.

7. A large and growing addressable market

Underpinning all of this is sheer scale. Roughly 95 million US households own a pet, which keeps broadening the addressable market for everyone in the ecosystem.

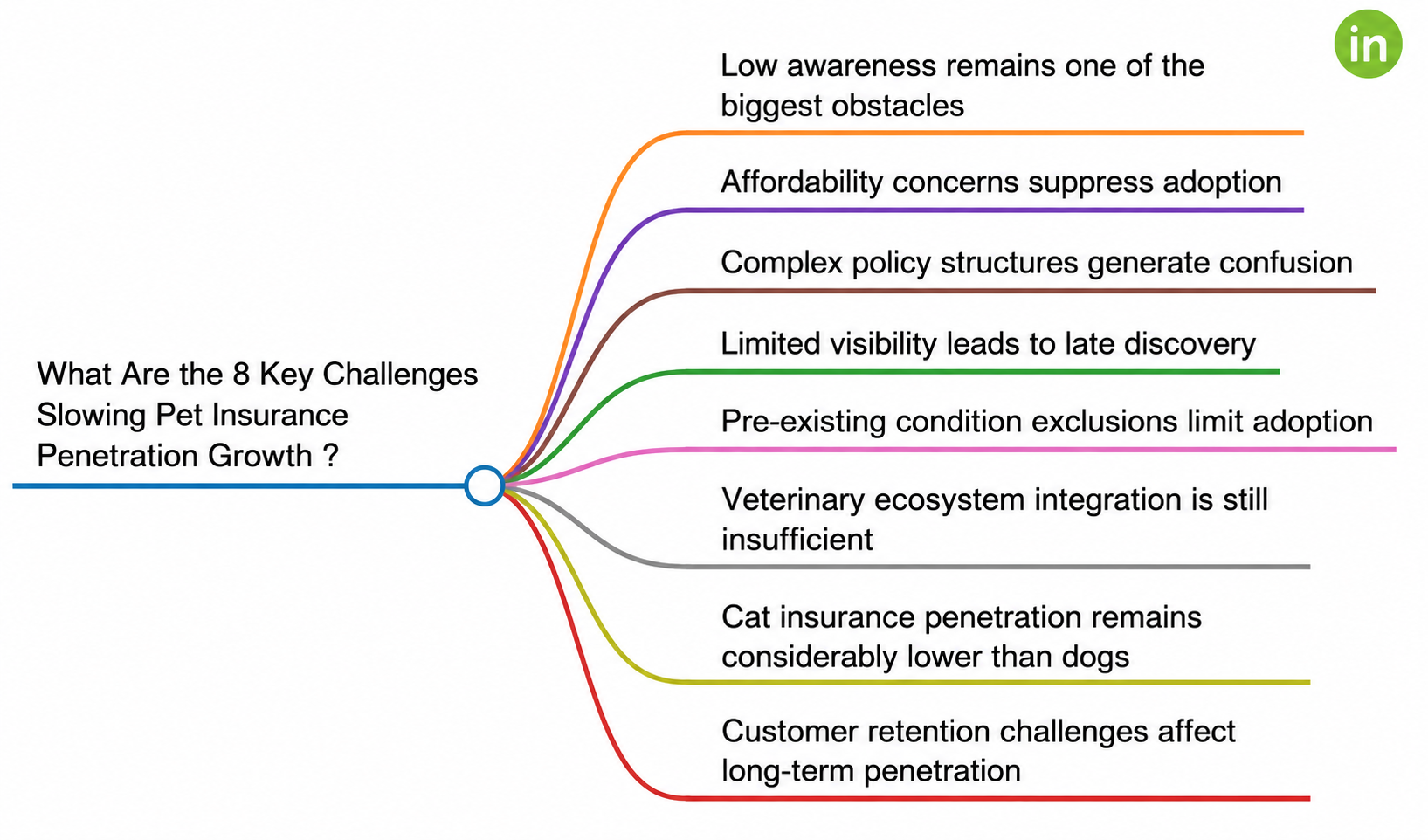

What Are the 8 Key Challenges Slowing Pet Insurance Penetration Growth?

Even with strong tailwinds, several persistent challenges prevent the market from scaling as fast as it could.

1. Low awareness remains one of the biggest obstacles

Many owners still do not understand how pet insurance operates, what expenses are covered, how reimbursement models function, or what the long-term financial value really is. Awareness here is considerably lower than it is for human health insurance.

2. Affordability concerns suppress adoption

Monthly premiums can appear costly, and rising veterinary inflation keeps pushing pricing higher. Multi-pet households face greater total costs, and cost-conscious customers frequently defer purchase due to budget pressure.

3. Complex policy structures generate confusion

Customers struggle to interpret different reimbursement structures, percentage-based reimbursement, annual deductibles, coverage limits, and waiting periods all add friction to an already challenging comparison.

4. Limited visibility leads to late discovery

Many owners find out about insurance too late, often only after their pet has already developed a medical condition. Coverage is not consistently presented during the key moments: pet adoption, veterinary onboarding, pet retail purchases, or wellness platform subscriptions.

5. Pre-existing condition exclusions limit adoption

Customers become frustrated when existing conditions are not covered. Late-stage purchase reduces a policy's usefulness and creates an impression that insurance offers limited value.

6. Veterinary ecosystem integration is still insufficient

Real-time connectivity between insurers, veterinary clinics, and claims systems remains weak. Manual invoice handling delays reimbursement, the absence of standardised veterinary data creates operational inefficiencies, and limited integration restricts how far automation can advance.

7. Cat insurance penetration remains considerably lower than dogs

Cat owners are less inclined to purchase insurance, often perceiving lower treatment urgency, and awareness is weaker in this segment. The result is uneven penetration growth across pet categories.

8. Customer retention challenges affect long-term penetration

Premium increases at renewal, cancellations after low claim utilisation, and broader economic pressure all weigh on renewals. Lower retention undermines sustainable, long-term penetration growth.

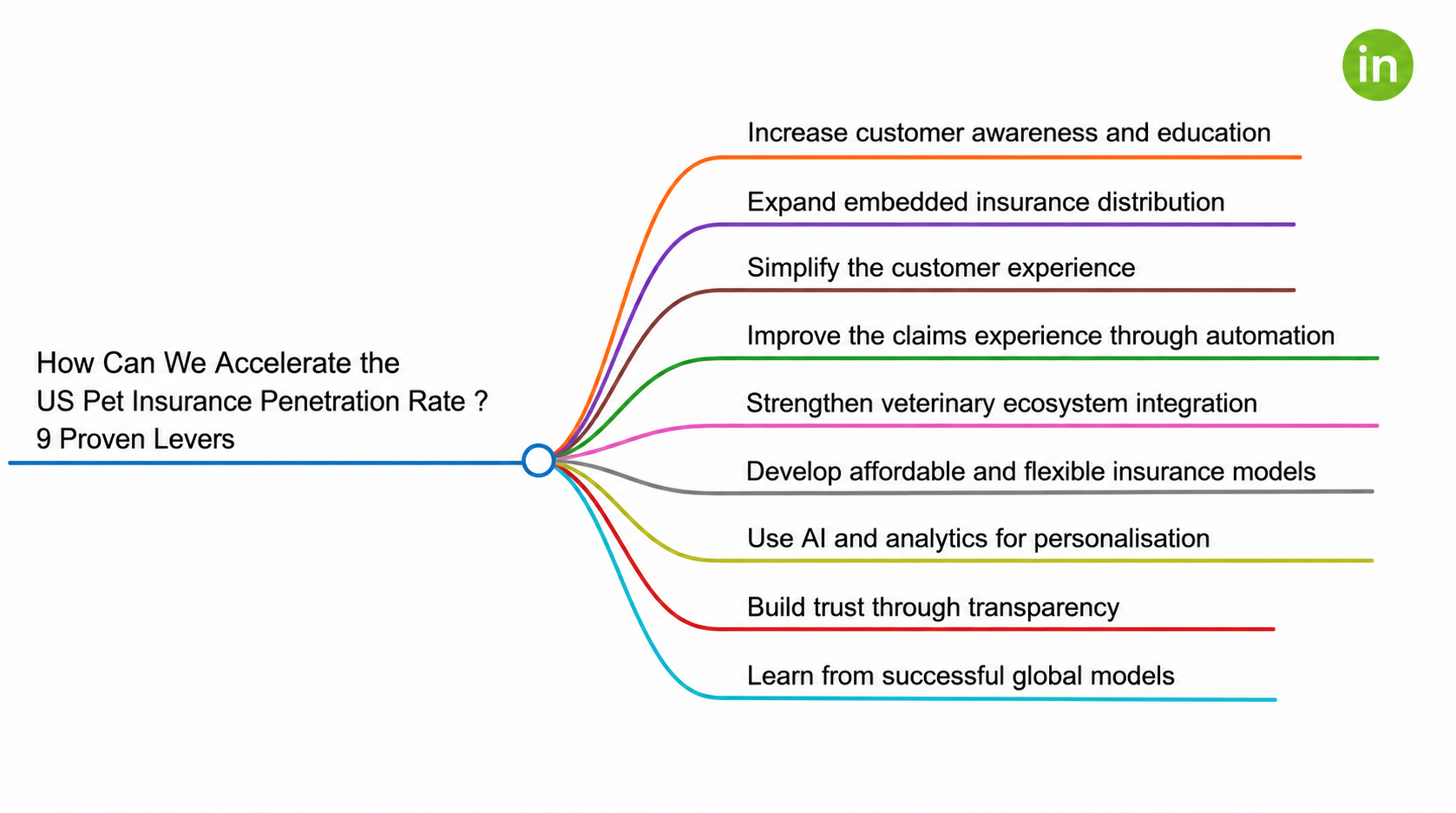

How Can We Accelerate the US Pet Insurance Penetration Rate? 9 Proven Levers

The barriers are clear and so are the remedies. Most of the levers are operational and within the industry's reach.

1. Increase customer awareness and education

Clarify how owners understand coverage, the claims process, reimbursement structure, and policy benefits. Develop educational campaigns through social media, veterinary clinics, pet influencers, and digital communities, and concentrate on building awareness during the early pet-ownership stage, before conditions emerge.

2. Expand embedded insurance distribution

Present insurance at the moments that count: pet adoption, veterinary onboarding, pet retail purchases, wellness subscriptions, and employer benefit programmes. Raising visibility at these high-intent touchpoints improves early-stage policy adoption.

3. Simplify the customer experience

Faster quote-to-bind journeys, mobile-first onboarding, self-service portals, straightforward policy comparison, and transparent pricing all lower friction. Simpler experiences directly improve conversion.

4. Improve the claims experience through automation

OCR-based invoice extraction, AI-assisted claims validation, real-time claim tracking, and faster reimbursement workflows reduce manual processing. A stronger claims experience is one of the most effective builders of customer trust.

5. Strengthen veterinary ecosystem integration

Establish real-time connectivity between insurers, veterinary clinics, and claims platforms. Direct vet payment systems, faster claims approvals, and better operational efficiency eliminate the "pay first, wait later" anxiety that holds buyers back.

6. Develop affordable and flexible insurance models

Multi-pet discounts, tiered coverage plans, subscription-style payment models, and wellness add-ons make coverage more reachable for a broader range of budgets.

7. Use AI and analytics for personalisation

Personalised coverage recommendations, risk-based pricing, preventive healthcare insights, and AI-driven underwriting make policies feel relevant to each customer, improving both fit and conversion.

8. Build trust through transparency

Clear policy wording, transparent claims communication, faster reimbursement, and stronger customer support accumulate over time. Trust-driven ecosystems are what sustain long-term penetration.

9. Learn from successful global models

Sweden built high penetration on early awareness and deep veterinary partnerships. Trupanion demonstrated the power of a direct vet payment experience. Lemonade showed what digital-first onboarding and AI claims can deliver. These global learnings can meaningfully accelerate US penetration growth.

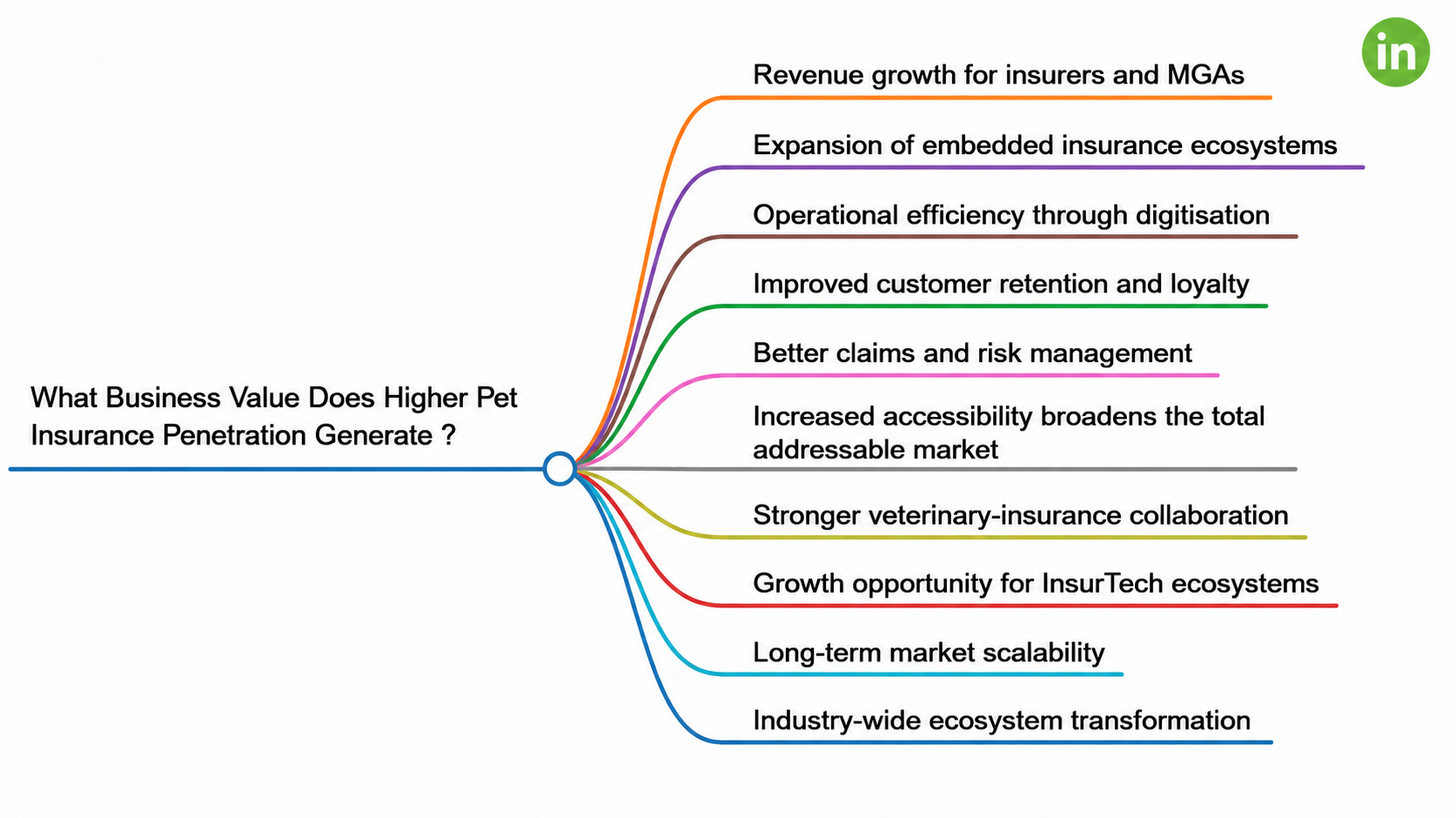

What Business Value Does Higher Pet Insurance Penetration Generate?

Closing the penetration gap is not just beneficial for pets and their owners. It unlocks real, structural value across the entire ecosystem.

1. Revenue growth for insurers and MGAs

A larger insured pet population increases premium volume, recurring subscription-style models generate predictable revenue, and higher customer lifetime value compounds over time. Pet ecosystems also open cross-selling opportunities that extend each customer relationship.

2. Expansion of embedded insurance ecosystems

Higher penetration is built on partnerships with veterinary clinics, pet retailers, wellness platforms, employer benefit providers, and pet adoption agencies. This ecosystem-driven distribution is what makes growth scalable rather than linear.

3. Operational efficiency through digitisation

AI underwriting reduces manual workload, OCR-based claims automation improves processing speed, and automation lowers operational costs overall. Faster workflows translate directly into more efficient servicing.

4. Improved customer retention and loyalty

Faster claims enhance satisfaction, transparency builds confidence, and digital servicing deepens engagement. Together, these reinforce long-term relationships and improve renewal rates, the foundation of sustainable penetration.

5. Better claims and risk management

AI-driven fraud detection, data-driven underwriting, personalised pricing, and predictive analytics all sharpen risk assessment, protecting margins as the book expands.

6. Increased accessibility broadens the total addressable market

Affordable pricing models attract wider customer segments, embedded distribution extends reach, and digital onboarding lowers friction, bringing more of the uninsured majority into the market.

7. Stronger veterinary-insurance collaboration

Faster payment systems improve the clinic experience, better claims integration enhances operational coordination, and veterinary partnerships raise policy visibility at the point of care.

8. Growth opportunity for InsurTech ecosystems

API-driven insurance infrastructure, embedded finance models, digital claims ecosystems, and real-time policy servicing platforms all stand to gain from rising penetration.

9. Long-term market scalability

With the majority of pets still uninsured, substantial future penetration opportunity remains, and early market participants can establish a durable competitive advantage.

10. Industry-wide ecosystem transformation

Ultimately, this represents a transition from the traditional reimbursement model toward a connected healthcare ecosystem, one defined by data-driven decision-making and an improved customer experience across the entire pet healthcare journey.

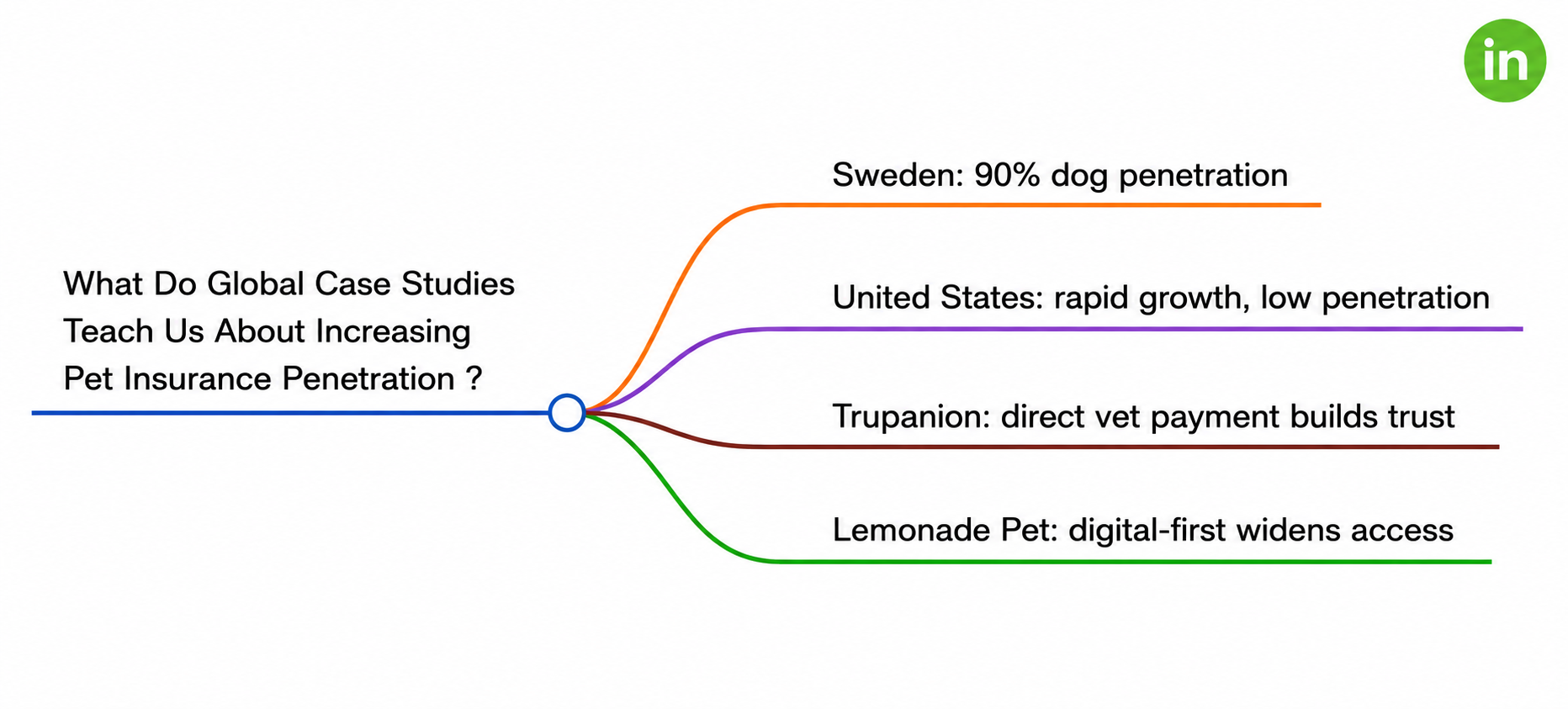

What Do Global Case Studies Teach Us About Increasing Pet Insurance Penetration?

The path forward is not theoretical. Around the world, specific markets and companies have already demonstrated what works.

1. Sweden: 90% dog penetration

With around 90% dog insurance penetration, Sweden is the global benchmark. Its achievement rests on a strong veterinary-insurance ecosystem and early customer awareness. The key lesson: early adoption and trust are what drive penetration to scale.

2. United States: rapid growth, low penetration

The US shows rapid market growth but still-low penetration, with a large uninsured pet population and a strong InsurTech ecosystem now emerging. The key lesson: market growth alone does not guarantee high penetration.

3. Trupanion: direct vet payment builds trust

Trupanion established its reputation on a direct vet payment system, a faster claims experience, and strong veterinary partnerships. The key lesson: faster reimbursements directly strengthen customer trust.

4. Lemonade Pet: digital-first widens access

Lemonade introduced fully digital onboarding, AI-assisted claims processing, and a mobile-first customer experience to the category. The key lesson: simpler digital journeys improve both accessibility and adoption.

Taken together, these examples point to the same conclusion: trust, simplicity, and well-timed distribution are what convert a growing market into a deeply penetrated one.

Conclusion

Pet insurance has moved from niche toward mainstream, but a 3.92% US pet insurance penetration rate tells us the market is still in its early stages. The growth drivers are structural and durable: rising veterinary costs, pet humanisation, a digitally native generation of owners, and an addressable base of roughly 95 million pet-owning US households. What is holding penetration back is not demand. It is friction in awareness, affordability, policy clarity, claims trust, and distribution timing.

The good news is that nearly every one of those barriers is resolvable, and most of the levers sit within the industry's own reach. Education delivered at the right moment, embedded distribution at high-intent touchpoints, simpler buying journeys, automated and transparent claims, deeper veterinary integration, flexible pricing, and AI-driven personalisation are not aspirational. They are already being executed by the market's most successful participants.

The global evidence is clear. Sweden shows what is achievable when awareness and trust are built early. Trupanion shows that faster reimbursement wins loyalty. Lemonade shows that simpler digital journeys broaden access. The common thread: market growth alone does not guarantee penetration. Trust, simplicity, and timely distribution do.

For carriers, MGAs, brokers, and InsurTech players, this is the opportunity of the decade. More than 96% of US pets remain uninsured. The demand exists, the technology exists, and the addressable market is enormous. The winners will be the ones who make pet insurance easy to understand, easy to buy at the right moment, and easy to claim. The players who build that connected, customer-first infrastructure today will define the pet insurance penetration rate of tomorrow.

Frequently Asked Questions

What is the current US pet insurance penetration rate?

The US pet insurance penetration rate reached 3.92% in 2024, meaning more than 96% of pets remain uninsured. Dog penetration stands higher at around 5.46%, while cat penetration trails at just 2.04%, pulling the overall average down.

Why is US pet insurance penetration still below 4%?

Penetration stays below 4% due to a combination of low consumer awareness, affordability concerns, complex policy structures, limited visibility at the right purchase moments, pre-existing condition exclusions, claims distrust, and fragmented veterinary ecosystem integration.

What is driving pet insurance adoption growth in the US?

Rising veterinary costs, pet humanisation, improving digital distribution, InsurTech automation, employer benefit programmes, and a large growing addressable market of roughly 95 million US pet-owning households are the primary growth drivers.

How does embedded insurance help increase pet insurance penetration?

Embedded insurance places coverage offers at high-intent moments like pet adoption, vet visits, pet retail purchases, and wellness subscriptions. Increasing visibility at these touchpoints improves early-stage adoption before conditions develop.

Why is cat insurance penetration lower than dog insurance?

Cat penetration sits at just 2.04% compared to dog penetration at around 5.46%. Cat owners tend to perceive lower health risk and less urgency, and awareness is significantly lower in this segment, dragging down overall penetration numbers.

What are the biggest challenges slowing pet insurance penetration growth?

The key challenges are low consumer awareness, affordability pressure, policy complexity, late discovery of insurance, pre-existing condition exclusions, limited veterinary ecosystem integration, and customer retention pressure at renewal.

How can insurers and MGAs speed up pet insurance penetration?

The 9 key levers are: increase awareness and education, expand embedded distribution, simplify the buying experience, automate claims, strengthen veterinary integration, develop flexible pricing models, use AI for personalisation, build trust through transparency, and learn from successful global models like Sweden and Trupanion.

Which global markets have achieved high pet insurance penetration?

Sweden leads globally with around 90% dog insurance penetration, built on early awareness and deep veterinary partnerships. In the US, Trupanion proved that direct vet payment builds trust, and Lemonade demonstrated that digital-first onboarding widens adoption.