Pet Insurance Customer Complaints: What Thousands Reveal and How to Fix the 96% Gap

Why Does a $5.2B Pet Insurance Market Still Leave 96% of Pets Uninsured?

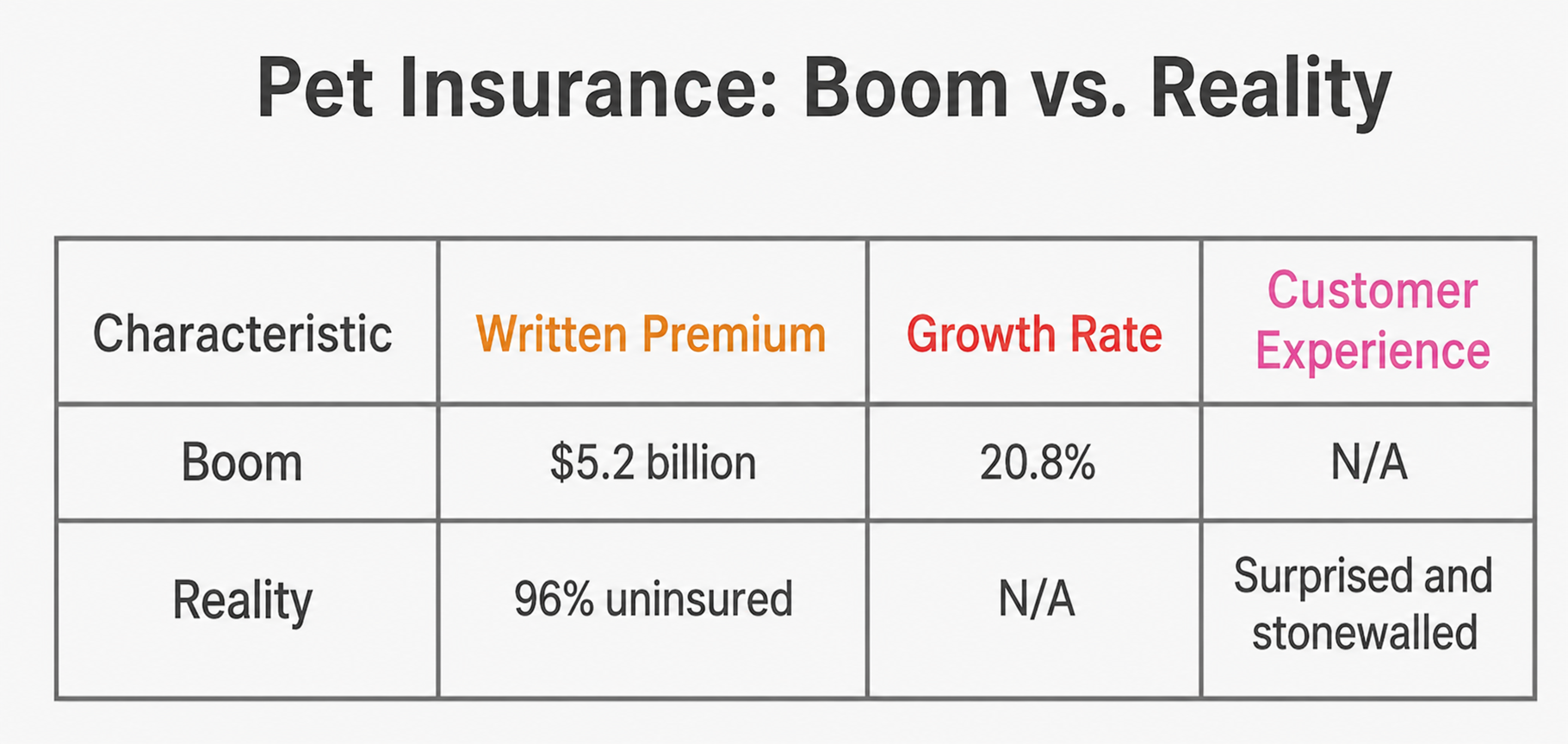

Because the barrier isn't price: it's trust. Owners don't doubt that pets get sick; they doubt the policy will actually pay when it does. North American pet insurance written premium crossed $5.2 billion at the end of 2024, up 20.8% in a single year, according to NAPHIA, and yet an estimated 96% of U.S. pets remain uninsured, a gap explored in depth in our pet insurance penetration rates analysis. Read enough pet insurance customer complaints and the contradiction resolves itself: owners aren't rejecting insurance, they're rejecting being surprised and stonewalled at the worst possible moment, with a sick pet and a vet bill in hand. We analyzed thousands of these reviews, and beneath the anger sits a single, fixable pattern. For the MGAs, carriers, agencies, and operators building this category, that pattern is the clearest map you have to the 96% still sitting on the sidelines.

What Do Most Pet Insurance Customer Complaints Have in Common?

Almost every complaint reduces to the absence of one of three things, and almost every fix is an application of them.

Transparency shows the why. Not "your premium is now $480," but "it rose $60 as your pet aged and $30 from vet-cost inflation."

Coaching guides customers toward better outcomes the way a credit-score app does: "stay claim-free and complete a dental cleaning, and here is how your rate improves."

Prevention uses data to stop problems before they start, spotting a breed's likely condition and offering screening before the costly claim ever happens. Hold these three in mind as you read what owners are actually angry about, what each complaint costs you, and how technology closes the gap.

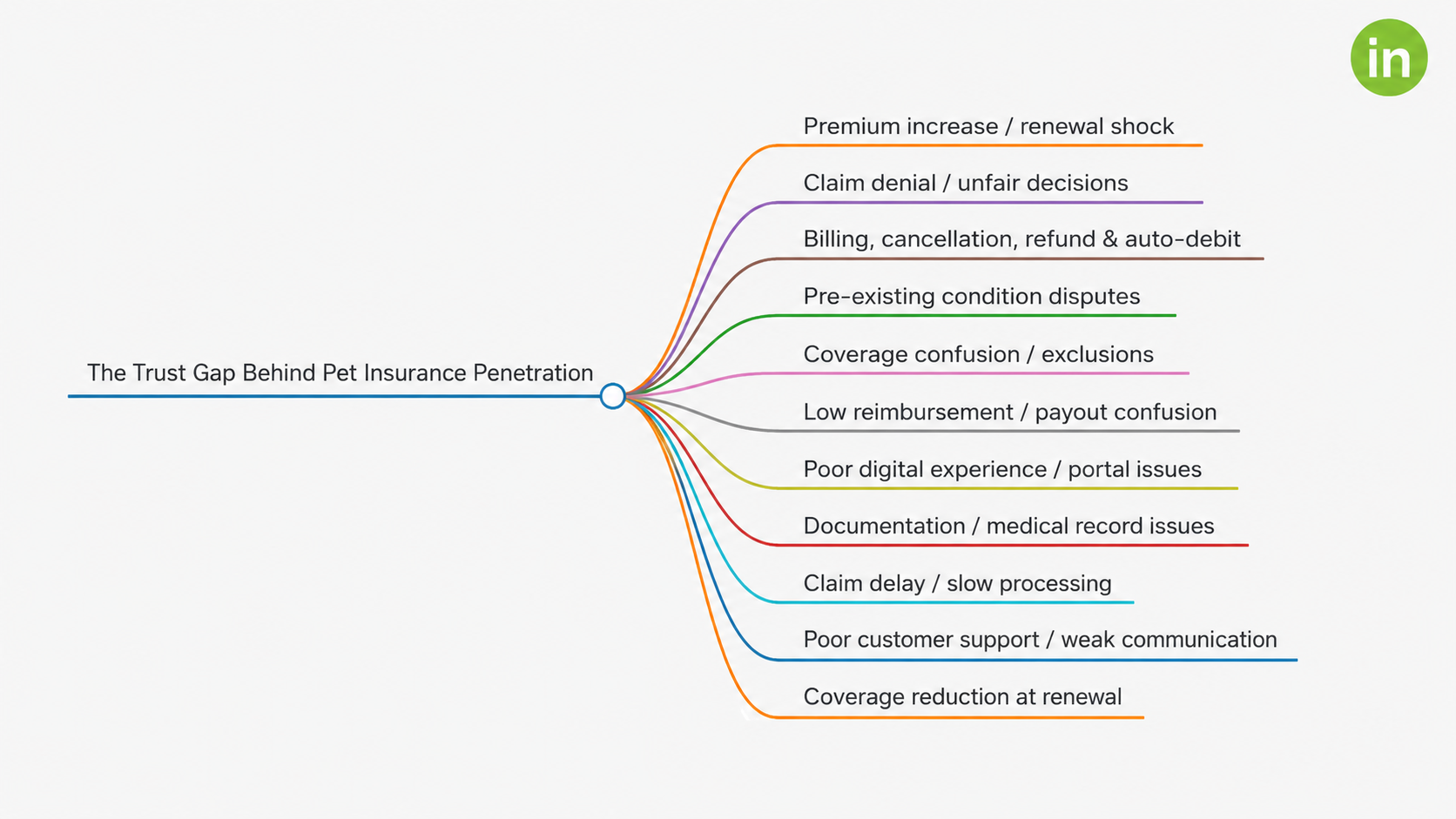

What Are the 11 Most Common Pet Insurance Customer Complaints?

The 11 most common pet insurance customer complaints are premium increases and renewal shock, claim denials that feel arbitrary, billing and cancellation friction, pre-existing condition disputes, coverage confusion and hidden exclusions, low or unexplained reimbursements, clunky digital and portal experiences, repeated documentation requests, slow claim processing, weak customer support, and coverage that quietly shrinks at renewal. Across thousands of reviews, nearly every one traces back to the same root cause: customers feeling surprised or stonewalled at the exact moment they need the policy. The sections below break down each one into the problem owners describe, its business impact on carriers and MGAs, and the technology fix that closes the gap.

1. Premium increase and renewal shock

The problem: A premium jumps at renewal, after a claim, as the pet ages, or after a portfolio re-rate, and the bill arrives with a new number and no breakdown. The owner cannot tell whether they are being penalized for using the policy, repriced for genuine risk, or simply absorbing vet-cost inflation. Because nothing explains the jump, it reads as arbitrary and punitive. For a product bought entirely on trust, an unexplained increase is the fastest way to make a loyal customer feel exploited.

Business impact: Renewal is the single biggest churn moment in the book, and an unexplained hike is exactly what triggers the comparison shop, which is why MGA retention strategies must start well before the renewal notice arrives. When a customer walks in year two or three, you forfeit the multi-year lifetime value that finally turned that acquisition cost profitable. Worse, the churned customer often posts a public complaint, which raises acquisition cost for every prospect behind them. A few points of avoidable renewal churn compound into a structural drag on growth.

The solution: Itemize every increase: this much for age, this much for claims, this much for vet-cost inflation, this much for breed, so the number has a visible cause. Flag the likely rises at the point of sale so renewal becomes a confirmation, not an ambush. Add a credit-score-style tool that shows customers how staying claim-free or completing preventive care improves their rate, powered by AI retention prediction models that identify at-risk policies before the renewal window opens. Then fund breed-level digital prevention, informed by breed risk scoring, so the underlying claim cost, and therefore the premium itself, actually comes down over time.

2. Claim denial and unfair decisions

The problem: A claim the owner is certain is valid comes back denied, and the reason only appears after they have already paid the vet out of pocket. Because the logic is opaque and arrives too late to act on, the "no" feels less like a policy decision and more like a refusal to pay. The owner experiences it at the exact moment of maximum stress, a sick pet and a bill, which amplifies the sense of betrayal. With no clear path to understand or contest it, the denial becomes the story they tell everyone.

Business impact: The claim is your product's moment of truth; it is the one time the customer discovers whether the policy was ever real. A denial that feels unfair does not just lose that customer, a pattern MGA denial rate benchmarks confirm across the industry; it produces the one-star reviews that prospective buyers read before they request a quote. In a category where 96% are still uninsured and skeptical, denial reviews directly throttle the top of your funnel. Each avoidable bad-feeling denial is paid for many times over in lost new business.

The solution: Give every decision a plain-language "receipt" that states the exact clause, the exact reason, and the evidence that drove it, the way an explanation of benefits generator does automatically for every adjudicated claim. Add a pre-claim "Will this be covered?" checker, such as a coverage Q&A chatbot, so owners learn the answer before they are standing at the vet counter. Mine your denial data to surface the root causes (confusing wording, a common exclusion, a documentation trap) and fix them at the source. A denial that is understood is survivable; a denial that feels arbitrary is not.

3. Billing, cancellation, refund, and auto-debit

The problem: Unexpected charges, auto-debit failures, refunds that never seem to arrive, and cancellations that require a phone call and a fight quietly erode trust between claims. Customers who cannot change a payment date, pause, or downgrade on their own are forced into support queues for tasks that should take ten seconds. When a card expires and the policy silently lapses, the owner only discovers it at claim time, when the consequence is catastrophic. None of this is dramatic on its own, but together it tells the customer the company is hard to deal with.

Business impact: Billing friction is a leading cause of involuntary churn: policies that lapse not because the customer chose to leave, but because a payment quietly failed. Failed payments and disputed charges generate chargebacks, which carry processor fees and risk on top of the lost premium. Every avoidable billing question is a support contact you pay for, inflating cost-to-serve across the entire book. And a customer who had to fight to cancel will not come back, and will say so publicly.

The solution: Give customers one clear billing ledger and a self-service panel where they can pause, cancel, change the payment date, downgrade, or track a refund without ever calling. Add AI chat and voice so routine billing questions resolve instantly, at any hour. Predict failed payments (expiring cards, insufficient-funds patterns) and reach out before the policy lapses rather than after. Making it easy to leave is, paradoxically, what makes customers stay.

4. Pre-existing condition disputes

The problem: At claim time, an old line buried in the vet record gets the condition branded "pre-existing," and the claim is voided. To the owner, coverage they had been faithfully paying for simply evaporated the moment they needed it, a scenario detailed in our pre-existing condition disputes guide. Often the note is ambiguous (a one-time symptom years ago, not a diagnosis), yet it is enough to deny. Because the determination happens after enrollment and after payment, it feels like a trap that was always going to spring.

Business impact: Pre-existing disputes draw the angriest reviews in the category and attract the most regulatory and media scrutiny. They do not just lose the customer; they poison the referral, because the owner warns every other pet parent they know. For an MGA or carrier, a visible pattern of these complaints is a reputational liability that can threaten distribution and partner relationships. The lifetime value lost on the policy is dwarfed by the acquisition value destroyed downstream.

The solution: Show the owner exactly what triggered the flag (which record, which date, which note) so the decision is contestable and transparent rather than a black box. Use AI to detect pre-existing conditions at enrollment, so expectations are set before the first premium, not after the first claim. Display what is and is not covered in plain terms at the point of sale. Finally, track conditions that requalify after a defined symptom-free period, and proactively tell the customer when coverage is restored.

5. Coverage confusion and exclusions

The problem: Most owners do not truly understand what their policy covers or excludes until they are at the vet with a claim in hand, and by then the gap is a surprise, not a choice they made. Dense policy language, undisclosed sub-limits, and waiting periods hide the real shape of the coverage. The customer believed they bought broad protection; they discover they bought a much narrower thing. The mismatch is rarely malice, but it lands as one.

Business impact: Coverage that does not match expectations becomes a cancellation and, increasingly, a mis-selling complaint that regulators take seriously. Every confused customer is both a churn risk and a brand risk, telling others that the product is misleading. Mis-set expectations also distort your loss experience, because customers end up buying the wrong plan for their pet. The cost shows up as lapses, complaints, and remediation, all of it avoidable.

The solution: Rewrite the policy in plain language a non-expert can act on, with exclusions and limits surfaced rather than buried. Add a coverage simulator that lets buyers test real scenarios (a dental procedure, an ACL tear, an allergy workup, an emergency surgery) before they purchase. Personalize plan recommendations from breed and age data so each customer is steered toward coverage that fits their actual risk. When expectations are set correctly up front, claims stop feeling like betrayals.

6. Low reimbursement and payout confusion

The problem: The payout lands far below the bill, and because the math behind it is invisible, the owner assumes they were shortchanged. Deductibles, co-insurance percentages, benefit schedules, and per-condition caps all quietly reduce the check, but none of it is shown. The customer did everything right (paid premiums, filed the claim) and still feels out of pocket. Without the calculation laid out, a perfectly legitimate payout looks like a rip-off.

Business impact: Payout disappointment is one of the top reasons customers lapse, and one of the most common warnings in reviews: "it isn't worth it." That single phrase, repeated across review sites, is corrosive to a category still trying to prove its value to the 96% uninsured. Each disappointed payout is both a churned customer and a public argument against buying pet insurance at all. The damage extends well past the individual policy.

The solution: Show the full payout math (bill, covered amount, deductible, co-insurance, applied limits) so the number is understood, not suspected. Add a pre-claim payout estimator, backed by a claim settlement calculation agent, so owners know roughly what to expect before they file. Use claims and vet-cost data to recommend a better deductible or reimbursement level at renewal, so the plan fits the customer's real spending. A payout that is explained is accepted; a payout that is mysterious becomes a one-star review.

7. Poor digital experience and portal issues

The problem: Customers stall on basic tasks (logging in, uploading a document, tracking a claim, cancelling) and end up calling support for things the portal should handle on its own. Clunky flows, broken uploads, and no claim visibility turn simple interactions into friction. At the buying stage, the same friction kills conversions before the first premium is ever paid. A digital product that feels broken signals an operation that is.

Business impact: Friction at purchase suppresses conversion, so paid traffic and partner referrals leak straight out of the funnel. Friction after purchase drives avoidable support volume and early churn, lengthening both cost-to-serve and acquisition payback. For MGAs competing on experience, a weak portal is a structural disadvantage against digital-native rivals. The lost efficiency compounds across every single policy in the book.

The solution: Show claim status like an order tracker, so customers can see exactly where they stand without calling. Unify policies, claims, billing, medical records, and support tickets in one self-service customer portal. Analyze portal usage to find precisely where customers drop off, and fix those specific steps. A portal that handles the routine work frees your humans for the cases that genuinely need them.

8. Documentation and medical record issues

The problem: Records get requested repeatedly, lost in transit, or rejected for missing fields, turning a single claim into a paperwork loop. The owner chases their vet for documents, submits them, and is then asked again, sometimes more than once. Each round adds delay while the pet is sick and the bill sits unpaid. What should be one clean transaction becomes a frustrating, open-ended task.

Business impact: Repeated document requests are a direct driver of claim cycle time, and slow claims strongly predict cancellation. Every extra round of back-and-forth is additional support cost and another opportunity for the customer to give up entirely. Claim abandonment looks like savings on paper but is actually churn in disguise, plus a bad review on the way out. The paperwork loop quietly raises both cost and attrition at the same time.

The solution: Build a Records Vault that stores the pet's medical history once, so it never has to be re-collected for every new claim. Give a case-based document checklist so customers know exactly what is needed up front. Use OCR and AI to read records, flag missing fields, and request them automatically before they cause a delay. Removing the paperwork loop both speeds the claim and eliminates a top source of complaints.

9. Claim delay and slow processing

The problem: Claims and appeals drag on for weeks with no status and no estimated decision date, leaving the owner anxious and out of pocket the entire time. The silence is the worst part: with no visibility, customers assume the worst and keep calling to check. The wait coincides with the most stressful moment: a recovering or sick pet and an unpaid bill. Speed and transparency are what the customer is really buying, and in these cases both are missing.

Business impact: Slow claims are one of the strongest predictors of cancellation, as claims processing time benchmarks confirm, and one of the most common complaints in reviews. Every anxious customer calls to check status, multiplying cost-to-serve on a claim that is already pending. Delay also damages the brand at exactly the moment the customer is deciding whether the product was worth it. In a trust-starved category, slowness reads as either incompetence or bad faith.

The solution: Show an expected-decision (SLA) tracker so customers always know when to expect an answer. Add a pre-submission completeness checker so claims arrive ready to adjudicate instead of missing pieces. Route simple, clean claims to automated approval via AI claims triage and reserve human review for the genuinely complex ones. Fast, visible claims turn the moment of truth into the proof point the product badly needs.

10. Poor customer support and weak communication

The problem: No callbacks, generic copy-paste replies, long holds, and no way to escalate leave customers feeling ignored at the worst possible time. The owner repeats their story to each new agent and still gets nowhere. Without an owner, a status, or a clear next step, a solvable issue festers into a full grievance. The support experience quietly tells the customer how much the company actually cares.

Business impact: Weak support converts fixable problems into cancellations and public complaints, and raises cost per contact through repeat calls. A single mishandled interaction during a claim can undo years of otherwise fine service. For decision-makers, support quality is not a cost center to minimize but a retention lever to protect. Every ignored customer is a churned customer and a warning to the next prospect in line.

The solution: Show owner, status, SLA, and next action on every ticket, so nothing falls through the cracks. Use AI chat and voice up front to resolve routine issues instantly, backed by a claims status communication agent, with guaranteed human escalation for anything that needs it. Reach out proactively at the moments customers are most likely to need help (right after a claim decision, just before a renewal) instead of waiting for them to chase you. Support that is visible and proactive is the cheapest retention you can buy.

11. Coverage reduction at renewal

The problem: At renewal the reimbursement quietly drops, the deductible rises, or the limits shrink, so the customer pays the same or more for less, often without realizing it until a claim falls short. The changes sit buried in renewal paperwork that almost no one reads closely. The owner discovers the weaker terms at the worst time, mid-claim, and feels deceived. Silent downgrades break trust precisely because they are silent.

Business impact: Quietly weaker coverage drives renewal churn and "felt cheated" reviews, eroding the lifetime value you spent years building. When the discovery happens at claim time, it compounds with denial and payout anger into the most damaging kind of complaint. These customers leave loud, warning others against the brand on the way out. The short-term margin from a quiet downgrade rarely covers the long-term cost.

The solution: Show a clear old-versus-new comparison at renewal, so any change in coverage is visible and chosen rather than hidden. Add a renewal advisor that explains what changed and why, and reward claim-free loyalty instead of penalizing it. Predict in advance how rising claim volume or a pet's age may pressure coverage, and have that conversation early. Transparency at renewal turns a churn trigger into a trust-building moment.

How Can Carriers and MGAs Turn Pet Insurance Complaints Into Growth?

The pet insurance customer complaints all tell one story:

owners are not leaving because the product costs too much; they are leaving because they feel kept in the dark.

Penetration is stuck near 4% for lack of trust, not lack of demand, and that makes it the most fixable problem in the industry.

Explain the decision, coach the customer, and use data to prevent the next problem.

For carriers, MGAs, and agencies, this turns customer experience from a cost center into the single biggest growth lever you have, as the customer experience innovations reshaping pet insurance MGAs already prove, and the operators who show their work, coach proactively, and earn that trust will be the ones who finally reach the 96% still on the sidelines.

Conclusion

Read across all eleven and the pattern is impossible to miss: pet insurance customer complaints are rarely about money. They are about the moment a customer reaches for the product they paid for and feels the door quietly close: an unexplained premium, a denial with no reason, a payout that does not add up, a claim that vanishes into silence. Every one of these is a trust failure, and trust is the one thing the category cannot afford to lose while 96% of owners are still deciding whether insurance is worth buying at all.

That is exactly why this is the most fixable problem in the industry. The answer is not a cheaper policy; it is transparency that shows the why, coaching that steers customers toward better outcomes, and prevention that stops the costly claim before it starts. The technology to deliver all three already exists, and the carriers, MGAs, and agencies that put it to work will convert their worst moments into proof points, while the rest keep funding their competitors one negative review at a time. The 96% are not waiting for a discount. They are waiting for a policy they can trust, and that is a gap you can close.

FAQs

What are the most common pet insurance customer complaints?

The most common pet insurance customer complaints are unexplained premium increases at renewal, claim denials that feel arbitrary, pre-existing condition disputes, slow claim processing, low or confusing reimbursements, and billing and cancellation friction. Nearly all of them trace back to a lack of transparency at the moment the customer needs the product most.

Why is US pet insurance penetration so low?

An estimated 96% of US pets remain uninsured, but the reviews show the barrier is trust, not demand. Owners are not rejecting insurance itself; they are reacting to being surprised and stonewalled at claim time. Penetration is stuck near 4% because customers do not trust that the product will pay when it matters.

Why do pet insurance customers cancel their policies?

Customers most often cancel at renewal, when an unexplained premium increase triggers comparison shopping, or right after a claim denial or disappointing payout that makes the product feel not worth it. The decision is rarely about absolute price; it is about feeling kept in the dark at the worst possible moment.

How can pet insurance MGAs and carriers reduce customer complaints?

By building three layers into the product: transparency that shows the reason behind every premium, denial, and payout; coaching that guides customers toward better outcomes like a credit-score app; and prevention that uses data to stop costly claims before they happen. Most complaints disappear when the why is made visible.

What causes pet insurance claim denials?

Most denials stem from pre-existing condition flags, policy exclusions, waiting periods, or documentation gaps that only surface after the owner has already paid the vet. The denial often feels arbitrary not because the decision is wrong, but because the reason is hidden and arrives too late to act on.

How does technology reduce pet insurance customer complaints?

Technology replaces opaque, slow, manual processes with plain-language decision receipts, pre-claim coverage and payout checkers, OCR-driven medical record handling, SLA claim trackers, and predictive prevention. It turns the moment of truth into a proof point instead of a complaint.

What is the biggest churn moment in pet insurance?

Renewal is the single biggest churn moment. An unexplained premium increase at renewal is what most often triggers a customer to shop competitors and cancel, erasing the multi-year lifetime value that finally made the original acquisition profitable.

How do pet insurance customer complaints affect new customer acquisition?

The claim is the product's moment of truth, and a denial or slow claim that feels unfair produces the one-star reviews that prospective buyers read before they ever request a quote. In a category where most pets are still uninsured, bad reviews directly choke top-of-funnel acquisition for everyone.