Pet Insurance Claims Process: What Pet Owners Actually Expect

What Pet Owners Want From the Pet Insurance Claims Process

Pet owners expect a pet insurance claims process that is transparent, fast, and supportive, not just a reimbursement check weeks later. They want an upfront coverage check, direct payment to the vet, live claim tracking, plain-language decisions, and a fair appeal. The claims process, not the sale, is where loyalty is won.

Why the claims process matters more than the sale

The claims process matters more than the sale because owners judge an insurer when they file a claim, not when they buy. That moment is stressful and high-stakes, so trust, clarity, speed, and support during the claim decide whether a customer renews, recommends, or leaves.

Pet insurance is growing because pet owners now see their pets as family members. They are willing to pay for insurance, but their real expectation from the pet insurance claims process starts when they file a claim. For them, the claim journey is not just about reimbursement. It is about trust, clarity, speed, and support during a stressful medical situation. In other words, the owner is judging the insurer at a moment when they are already under stress, and that is when trust, clarity, speed, and support matter most.

In pet insurance, claim rejection is one of the biggest pain points. Based on the data shared, claim rejection can be around 12%–18%, which means a noticeable number of pet owners may face claim denial, partial payment, or delay. Because each of those outcomes touches an owner during a difficult time, they weigh heavily on how the owner views the insurer. For MGAs, agencies, carriers, and pet insurance decision-makers, this creates an important question: how can the claim journey become more transparent, faster, and customer-friendly?

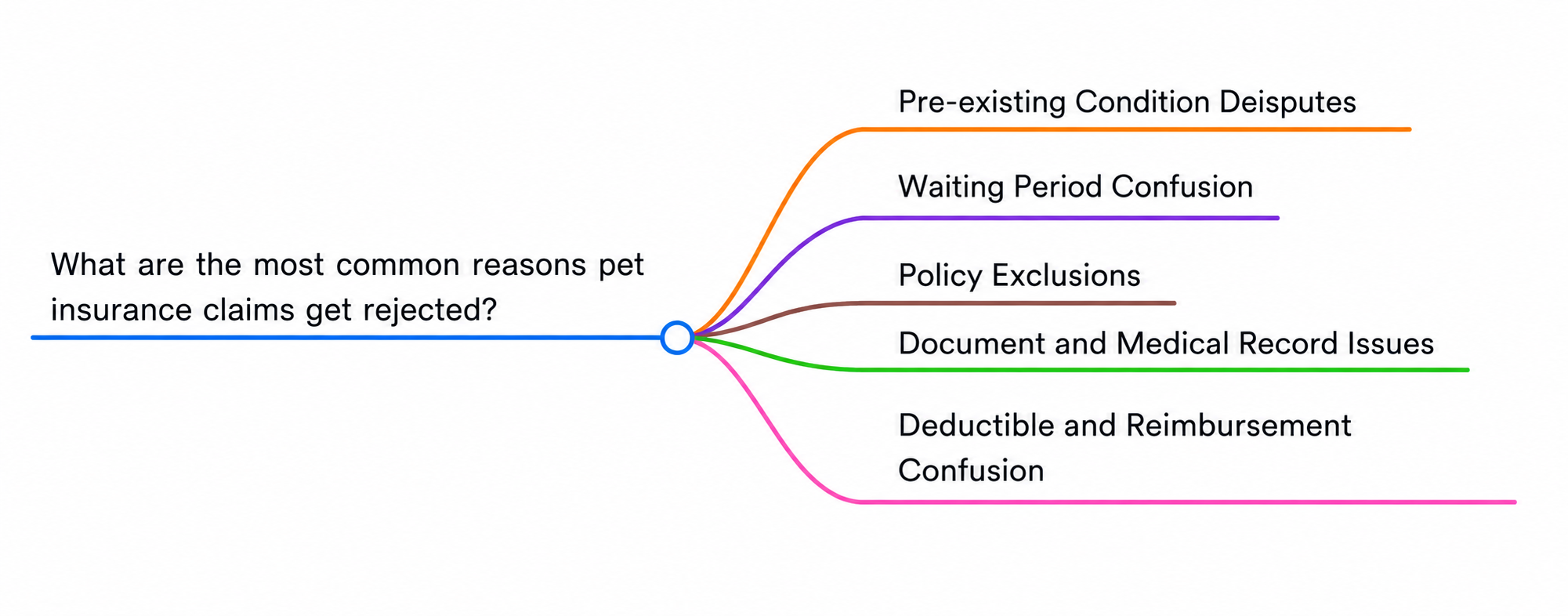

What are the most common reasons pet insurance claims get rejected?

Pet insurance claims are rejected most often for five reasons: pre-existing condition disputes, treatment inside a waiting period, policy exclusions such as routine or dental care, missing or incomplete documents, and unmet deductibles. Most trace back to the owner learning a rule only after filing.

Pet owners run into a set of recurring problems during the pet insurance claims process. Each one below is a point of friction that shapes the customer experience, explained in a little more detail.

1. Why are pre-existing conditions disputed in pet insurance claims?

Pre-existing conditions are disputed because the insurer links the current illness to old vet notes, earlier symptoms, or prior treatment the owner was not thinking about. The claim is denied on history the owner did not expect to matter, which is why it feels confusing.

This is one of the most common reasons for a pet insurance claim denial. The core issue is understanding: many pet owners do not clearly understand why a condition is considered pre-existing. When the insurer denies the claim based on old vet notes, earlier symptoms, or treatment history, the owner is left confused and frustrated, because the reason for the denial comes from information they were not thinking about when they filed.

2. How does the waiting period cause claim confusion?

The waiting period causes confusion when a claim happens too soon after the policy starts and the owner does not realize the treatment is not yet eligible. They feel they bought insurance but could not use it when they needed it. The issue is timing and awareness.

Sometimes the claim happens too soon after the policy starts, and the owner does not realize that the treatment is not eligible yet. The result is dissatisfaction: the owner feels they bought insurance but could not use it when they needed it. The problem here is timing and awareness, not the treatment itself. A well-structured claims handling workflow catches waiting-period claims early and communicates the reason clearly, rather than leaving the owner guessing.

3. What do pet insurance policy exclusions leave out?

Policy exclusions often leave out routine care, dental disease, vaccinations, exam fees, and hereditary conditions in the base policy. The problem is that many owners only learn about these exclusions after filing a claim, which is what makes the experience negative.

Certain treatments, such as routine care, dental disease, vaccinations, exam fees, or hereditary conditions, may not be covered in the base policy. The difficulty is that many owners only understand these exclusions after filing a claim. Learning about an exclusion at that point, rather than earlier, is what makes the experience negative.

4. How do document and medical record issues delay claims?

Document and medical record issues delay claims through missing documents, rejected invoices, incomplete vet notes, and disputes over how a record is read. The real frustration is that when one missing document stalls a claim, the owner expects clear guidance rather than repeated follow-up.

Claims also run into problems with missing documents, rejected invoices, incomplete vet notes, and how a medical record is interpreted. The frustration is not simply that a document is needed. It is that when a claim is delayed only because one document is missing, the owner expects clear guidance on what is needed, rather than repeated rounds of follow-up. Veterinary invoice OCR and AI tools now enable insurers to extract data from invoices and vet notes automatically, reducing the back-and-forth that slows claims down.

5. Why do deductibles and reimbursement limits confuse pet owners?

Deductibles and reimbursement limits confuse owners when the payout comes back lower than expected because the deductible was not met or the limit was reached. Even when the insurer calculated it correctly, the experience disappoints because the amount did not match what the owner expected.

An owner may file a claim expecting a payout, then later find that the deductible is not met, or that the reimbursement limit is lower than expected. Even if the insurer is technically correct in how it calculated the amount, the experience still feels disappointing, because the pet insurance reimbursement did not match what the owner was expecting.

Cut claim denials and disputes with Insurnest's pet insurance claims technology

Visit Insurnest to learn how we help MGAs, agencies, and carriers reduce friction across pre-existing checks, waiting periods, exclusions, and documentation.

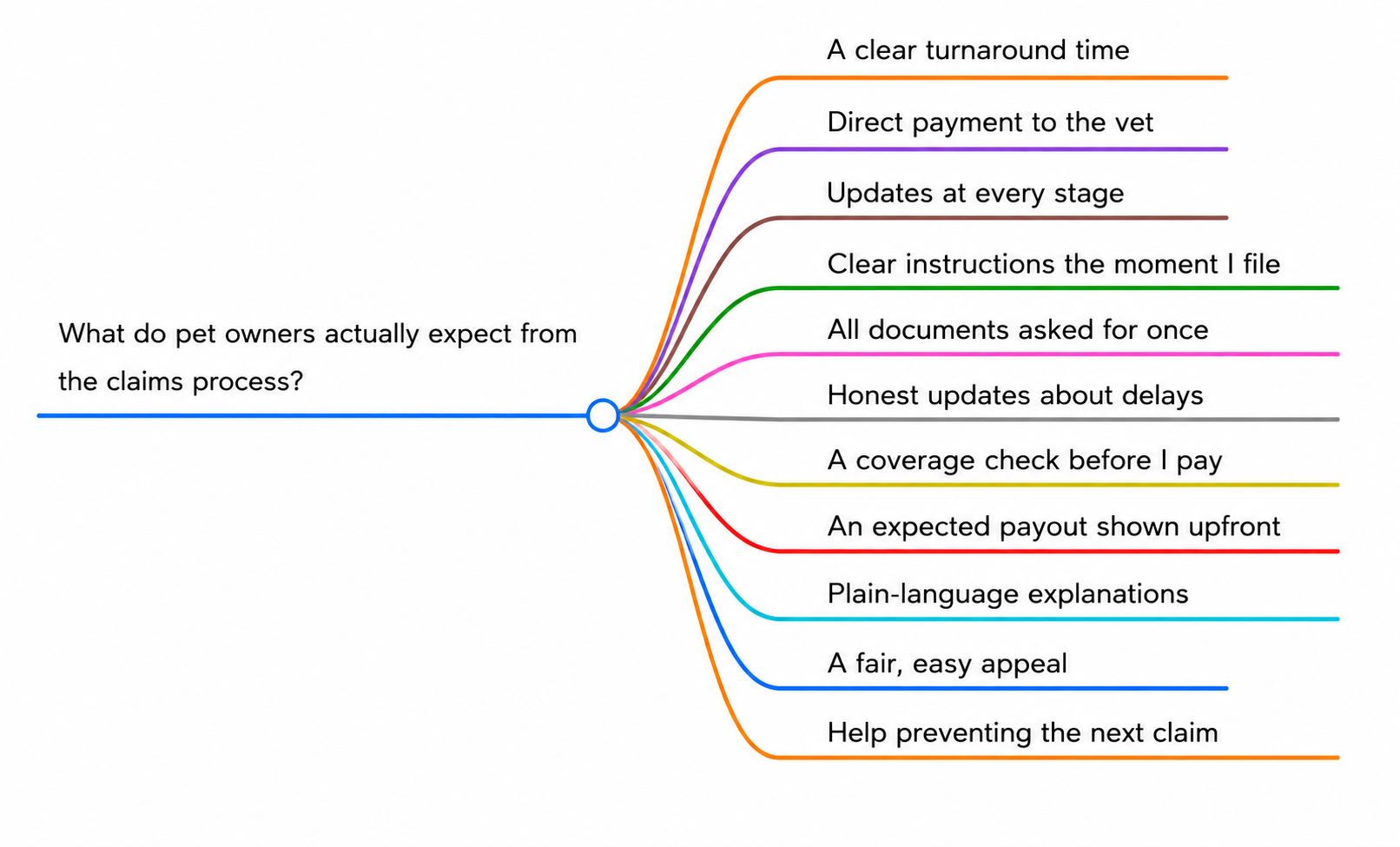

What do pet owners actually expect from the claims process?

Pet owners expect a coverage check before they pay, direct payment to the vet, live claim tracking, clear instructions at filing, documents requested once, honest delay updates, a payout estimate upfront, plain-language decisions, a fair appeal, and help preventing the next claim.

It is a Sunday night. Sarah's cat, Simba, has stopped eating and is breathing strangely. At the emergency vet, the doctor talks about tests, scans, maybe surgery, and a bill that could run into thousands. Standing in that bright, quiet waiting room, Sarah is not thinking about policy clauses or reimbursement percentages. She is thinking two things: Is Simba going to be okay? And quietly, guiltily: Can I afford to say yes to everything they recommend?

That second question is exactly where insurance is supposed to step in, where it should feel like a hand on the shoulder saying, "Go ahead, we've got the cost." Sarah does not want a reimbursement check three weeks later, after she has maxed out a credit card and chased three emails. In that moment she wants to know the treatment is covered, she wants the bill handled without floating the money herself, she wants to be told what happens next, and she wants to focus on Simba, not on paperwork.

That is the real expectation. Underneath the emotion sit a set of very concrete, very human asks. Here is what pet owners are really expecting from the claim experience, in their own words, with a little more on what each one means.

- A clear turnaround time. "Tell me when I'll get an answer and keep that promise." Owners can handle a wait; what they cannot handle is not knowing. A promised answer, kept, is what they are asking for. Research on claims processing time benchmarks shows that the timeline itself matters less than the certainty around it.

- Direct payment to the vet. "Pay the clinic directly, so I'm not floating thousands of my own money." The biggest stress is cash flow, not the final number. The ask is to not have to put up the full amount themselves.

- Updates at every stage. "Let me track my claim the way I track a parcel." Silence feels like the claim has been forgotten, so owners want to see where the claim is at each stage. A claims status communication system keeps the owner informed without them having to call.

- Clear instructions the moment I file. "When I submit, tell me exactly what happens next." The ask is to remove the guessing about steps, timelines, or what is needed, right at the point of filing.

- All documents asked for once. "Tell me everything you need in one go, not one new paper every three days." Repeated requests are the fastest way to lose trust, so owners want a single, complete request.

- Honest updates about delays. "If it's running late, tell me and tell me why." A proactive heads-up beats a silent wait every time, so owners want to hear about a delay before they have to chase it.

- A coverage check before I pay. "Tell me what's covered before I swipe my card, not after." Surprises at claim time feel like a broken promise, so owners want to know coverage upfront. A pre-authorization assistance system can confirm coverage before the owner pays.

- An expected payout shown upfront. "Show me roughly what I'll get back before I submit." This is what prevents the low-payout shock, so owners want an estimate before filing.

- Plain-language explanations. "Explain the decision like a human, not a policy document." This matters especially when the answer is no, because the owner still wants to understand the decision.

- A fair, easy appeal. "If I disagree, give me a real second look, not a dead end." The right to be heard rebuilds trust even after a denial, so owners want a genuine appeals process rather than a closed door.

- Help preventing the next claim. "Help me keep my pet healthy so we avoid the next emergency." Owners want a health partner, not just a payer, so they value help avoiding the next claim.

The real expectation, then, is not only a fast settlement. It is to feel guided and supported at every step, before, during, and after the claim.

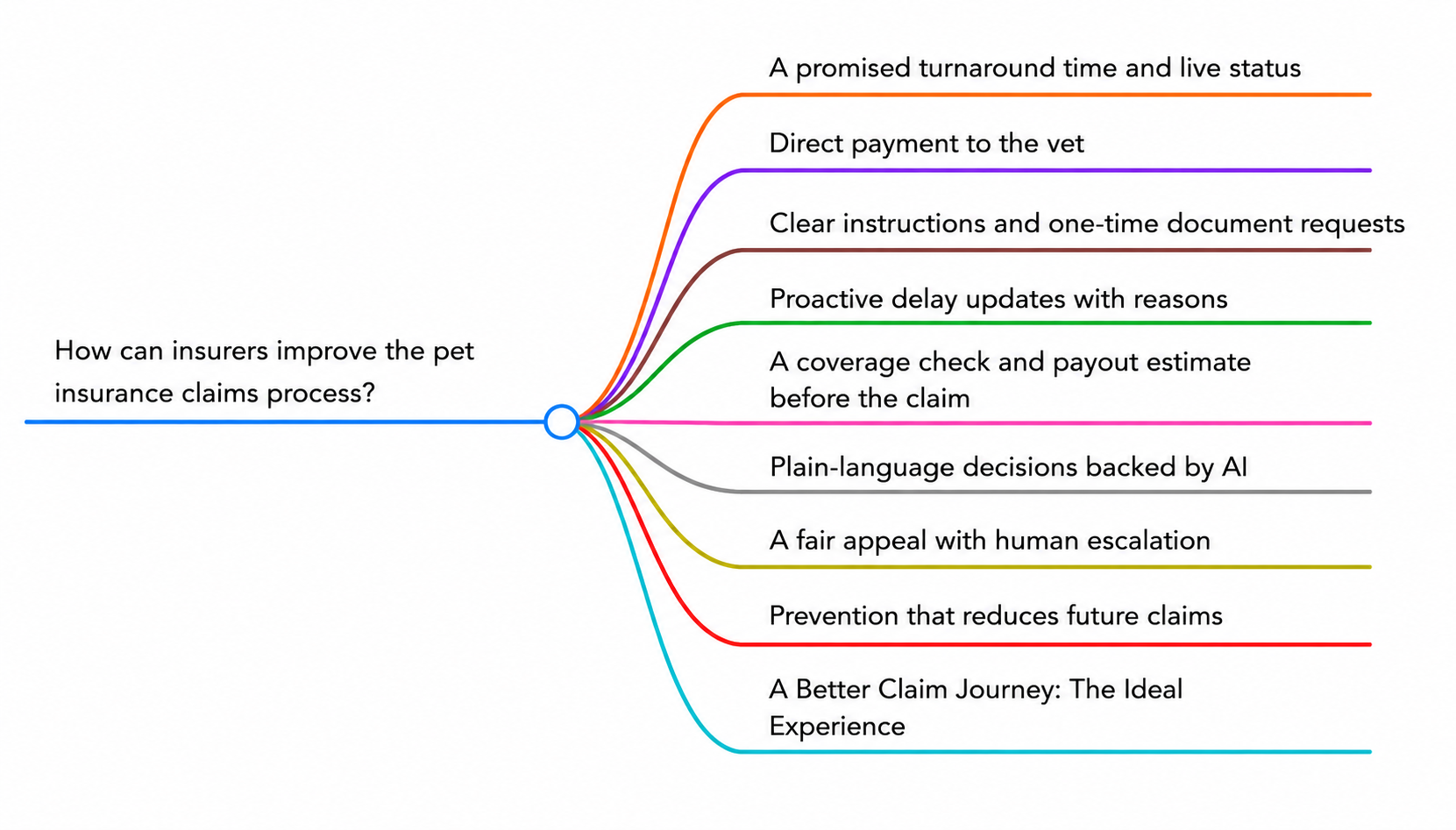

How can insurers improve the pet insurance claims process?

Insurers improve the pet insurance claims process by adding a claim tracker with an SLA, direct vet payment, guided one-time document requests, proactive delay alerts, upfront coverage and payout checks, AI plain-language decisions, a fair appeal workflow, and data-driven prevention.

This is where technology turns those expectations into reality. Each ask above maps to a capability an insurer can build into its claim management, described below in a little more detail.

1. How can insurers offer a promised turnaround time and live status?

Insurers offer a promised turnaround time by building a claim timeline tracker with a clear SLA that shows the expected decision date, the current stage, and the next action. It answers when a decision will come and where the claim stands, removing the silence owners dislike most.

A claim timeline tracker with a clear SLA shows the expected decision date, the current stage, and the next action, like an order tracker. It answers "when will I know?" and "where is my claim?" in one place, and removes the silence that frustrates owners most.

2. How does direct payment to the vet help pet owners?

Direct payment to the vet helps owners because the insurer settles its share with the clinic at checkout, so the owner pays only their portion and never floats the full bill. For many claims, this removes the reimbursement wait and the cash-flow stress entirely.

A vet direct-pay integration lets the insurer settle its share with the clinic at checkout, so the owner pays only their portion and never floats the full bill. For many claims, this removes the reimbursement wait entirely.

3. How can insurers give clear instructions and request documents once?

Insurers give clear instructions through a guided claim flow that tells the owner what happens next the moment they file. Paired with AI document extraction and a case-based checklist, the system identifies everything a specific treatment needs and asks for it all at once, not one paper at a time.

A guided claim flow tells the owner exactly what happens next the moment they file. An FNOL intake system captures the first notice of loss via chat, phone, or web, while claims automation paired with AI-based document extraction and a case-based checklist reads invoices and vet notes, identifies everything required for that specific treatment, and asks for it all at once instead of one document at a time.

4. Why should insurers send proactive delay updates?

Insurers should send proactive delay updates because a delay the owner is warned about, with a reason and a revised date, is far less damaging than one they discover by chasing. Automated notifications at each stage keep the owner informed and preserve trust even when the timeline slips.

Automated status notifications keep the owner informed at each stage and, crucially, flag any delay with the reason and a new expected date. A delay the owner understands is far less damaging than a delay they discover by chasing.

5. How can a coverage check and payout estimate prevent surprises?

A coverage check and payout estimate prevent surprises by confirming whether a treatment is covered, including waiting periods and exclusions, before the owner pays. A deductible tracker and payout estimator then show the expected reimbursement upfront, so the final number is never a shock.

A policy rule engine and coverage checker can confirm whether a treatment is covered, including waiting periods, exclusions, wellness, and add-ons, before the owner pays. A deductible tracker and payout estimator then show the expected reimbursement upfront, so the final number is never a shock.

6. How can AI deliver plain-language claim decisions?

AI delivers plain-language decisions through a medical record review system that reads vet notes, invoices, and history, then explains every decision in human-readable terms, including which note or date drove a pre-existing call. The owner gets a reason they can understand, not a coded denial.

An AI medical record review system reads vet notes, invoices, and history, and produces a clear, human-readable explanation of every decision, including exactly which note or date drove a pre-existing call. The owner gets a reason they can understand, not a coded denial.

7. What makes a fair pet insurance claim appeal?

A fair pet insurance claim appeal uses a workflow with SLA tracking so complex or disputed claims get a proper second look instead of being closed silently. It guarantees escalation to a real person for the hard or emotional cases, which preserves the owner's right to be heard.

An appeal workflow with SLA tracking ensures complex or disputed claims get a proper second look instead of being closed silently, with guaranteed escalation to a person for the hard or emotional cases.

8. How does prevention reduce future pet insurance claims?

Prevention reduces future claims by using claims and breed data to flag the conditions a pet is most likely to face and nudge timely preventive care such as screenings, dental, weight, and vaccinations. This keeps pets healthier, lowers future claims, and makes the insurer a trusted health partner.

Using claims and breed data, insurers can guide owners on the conditions their pet is most likely to face and nudge timely preventive care: screenings, dental, weight, vaccinations. Proactive wellness reminders keep pets healthier, lower future claims, and turn the insurer into a trusted health partner.

Build these claim capabilities faster with Insurnest's insurance-native technology

Visit Insurnest to see how we deliver claim tracking, vet direct-pay, coverage checks, and AI decisioning built from the insurance workflow up.

What does an ideal pet insurance claim journey look like?

An ideal pet insurance claim journey shows coverage and out-of-pocket cost upfront, pays the vet directly at checkout, accepts documents once, tracks the claim through each stage, delivers a plain-language decision, and follows up with preventive care reminders. The owner feels guided, never ignored.

Imagine Sarah's Sunday night again, but with all of this in place. At the clinic she opens the insurer's app and instantly sees that Simba's treatment is covered, the waiting period has passed, and her expected out-of-pocket cost. At checkout, the insurer pays the clinic directly, so she covers only her share. She uploads the invoice and notes once; the system confirms nothing is missing and shows her the steps ahead.

Over the next day she watches the claim move from received, to under review, to approved, without calling anyone. For an emergency like Simba's, a fast-track claims process can compress the timeline to hours rather than days. There are no surprise document requests and no silence. The claim approval arrives with a clear, plain-language breakdown of what was paid and why. A week later, a gentle reminder suggests a preventive check based on Simba's age and breed.

Sarah never felt ignored. She felt guided. That is the pet insurance customer experience owners are expecting, and the insurers who deliver it earn loyalty that price alone never could. A look at the end-to-end claims workflow shows how each of these pieces connects into a single, seamless journey.

Turn your claims process into a loyalty engine with Insurnest's pet insurance technology

Visit Insurnest to learn how we help MGAs, agencies, and carriers deliver direct vet payment, live claim tracking, and AI-driven claim decisions.

Conclusion

For carriers and MGAs, the pet insurance claims process is the strongest trust-building moment. Customers buy on price or coverage but stay because of the claim experience, so transparent decisions, fast document review, clear communication, direct payment, and prevention drive adoption and retention.

For insurance carriers and MGAs, the pet insurance claims process is the strongest trust-building moment. A customer may buy the policy because of price or coverage, but they stay with the insurer because of the claim experience.

To improve pet insurance adoption and retention, MGAs, agencies, and carriers need to focus on transparent claim decisions, faster document review, clear communication, direct payment, and prevention. The future of pet insurance claims is not only about paying faster. It is about making pet owners feel supported when they need help the most.

Frequently asked questions

Why do pet insurance claims get denied most often?

The common reasons are pre-existing condition disputes, treatment falling inside a waiting period, policy exclusions such as routine or dental care, missing or incomplete documentation, and unmet deductibles.

What is a pre-existing condition in pet insurance?

It is generally a condition tied to old vet notes, earlier symptoms, or treatment history from before the claim. Many owners do not clearly understand why a condition is considered pre-existing, which is why the denial feels confusing.

Can pet insurance pay the vet directly?

With a vet direct-pay integration, the insurer settles its share with the clinic at checkout, so the owner pays only their portion instead of floating the full bill and waiting for reimbursement.

How can owners avoid claim surprises?

A coverage check before paying, along with a deductible tracker and payout estimator, lets the owner see what is covered and roughly what they will get back before they file.

Can pet insurance help keep my pet healthy?

Yes. Using claims and breed data, insurers can nudge timely preventive care such as screenings, dental, weight, and vaccinations, which keeps pets healthier and lowers future claims.

How long does the pet insurance claims process take?

Timelines vary by insurer and by how complete the submitted documents are. What owners value most is a promised turnaround time backed by a clear SLA and live status updates, so they always know when a decision is expected and where the claim currently stands.

What should I do if my pet insurance claim is delayed?

Look for a status update explaining the delay and a revised expected date. A well-run claims process flags delays proactively with the reason, so owners are informed before they have to chase, rather than discovering the delay themselves.

How do I appeal a denied pet insurance claim?

Submit an appeal through the insurer's claims process, which should include an appeal workflow with SLA tracking so disputed or complex claims get a proper second look instead of being closed silently, with escalation to a person for the hard or emotional cases.

About the author

Hitul Mistry is the Founder of Insurnest, an InsurTech company that engineers end-to-end technology exclusively for the insurance industry serving carriers, TPAs, MGAs, brokers, and reinsurers across India, the UAE, and the US. With more than a decade of insurance domain experience, he has built systems spanning underwriting automation, AI-powered underwriting intelligence, claims management, rating and quoting, broking and agency platforms, and reinsurance automation across Health/GMC, Group Life, Motor, P&C, and Reinsurance. Insurnest doesn't adapt generic software to insurance; it builds from the workflow up.

Connect with Hitul on LinkedIn.