Pet Insurance MGA Digitisation: A Complete End-to-End Guide for the US Market

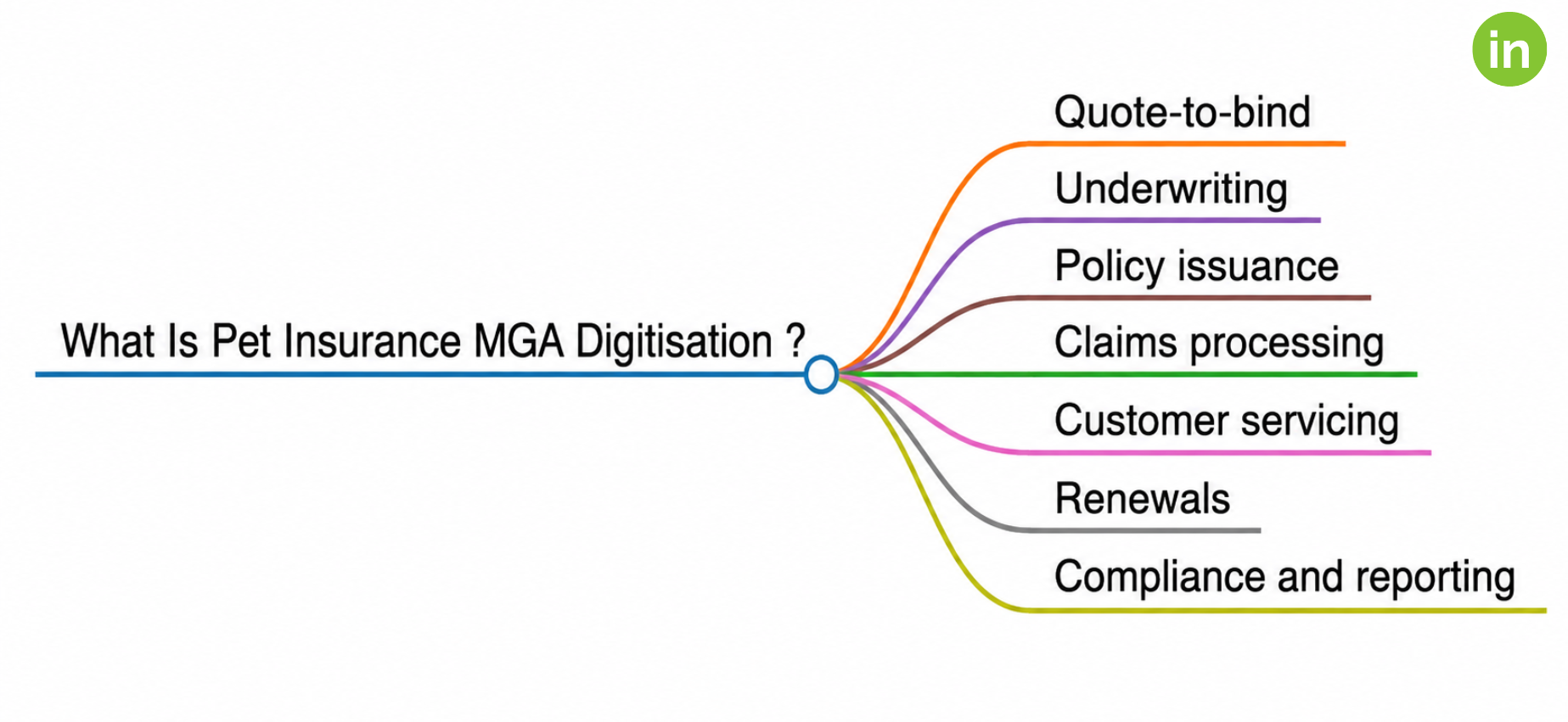

What Is Pet Insurance MGA Digitisation?

If you run a pet insurance MGA in the US, you already feel the pressure. Your book is expanding, your partners want faster onboarding, your carriers want cleaner data, and your customers expect an experience that matches what they get from every other app on their phone. Meanwhile, much of the operation still depends on email threads, PDFs, Excel trackers, manual underwriting, and manual claims review.

That setup holds at small scale. It quietly restricts your growth the moment you try to add carriers, expand distribution, or plug into embedded channels. Every manual handoff is a margin leak and a renewal risk.

Pet insurance MGA digitisation is how you break that ceiling and it means more than a customer portal. It means converting your entire lifecycle into connected, automated workflows that scale without scaling headcount. Here's where that plays out, and why each stage matters to your P&L.

1. Quote-to-bind own every point of sale

Your next policy won't always originate from your website. It comes from the vet clinic, the e-commerce checkout, the grooming chain, the telehealth visit, the daycare sign-up, the microchip registration. Direct-to-consumer, partner-led, and embedded journeys all need API-driven quoting that binds in the moment. The MGA that makes binding seamless at these touchpoints secures the policy before a competitor is considered.

2. Underwriting automate the clean, refer the complex

The majority of your risks are decidable on structured data: age, breed, pet type, gender, weight, location, pre-existing conditions, selected covers. Those should clear straight-through, instantly, with no human cost. Reserve your underwriters for the NSTP (Non-Straight-Through Processing, cases that require specialist review) like complex medical history, ambiguous pre-existing conditions, pet-photo risk signals, and fraud. This is how you grow volume without growing the underwriting team.

3. Policy issuance eliminate the handoffs

Core-system integration, automated email and SMS notifications, renewal reminders, digital signature binding, and real-time carrier notification. No re-keying, no delays, clean data flowing to your carriers automatically. This is the difference between a carrier viewing you as a liability or a preferred partner.

4. Claims processing protect retention where it's won or lost

Claims are the critical moment your customers judge you on. Digital FNOL (First Notice of Loss, the initial claim report submitted by the policyholder), automated investigation, AI-supported adjudication, and flexible payouts cashless directly to clinics, fast reimbursements to customers. Speed here is your single biggest lever on loss-ratio perception, renewals, and referrals.

5. Customer servicing self-service by default

A portal where customers handle claims, renewals, underwriting changes, and cross-sell or upsell themselves, supported across chat, call, email, and WhatsApp. Every interaction they complete without your team is cost saved and satisfaction gained.

6. Renewals automate the predictable

Proactive reminders, pre-filled offers, one-click confirmation. Renewal economics are the foundation of MGA profitability; automation protects them.

7. Compliance and reporting give carriers visibility they trust

Cloud-based analytics dashboards that give you and your carriers real-time visibility into the book. Transparency wins capacity.

Two forces make this transformation urgent right now. Embedded pet ecosystems are generating demand for insurance infrastructure that can plug in via API at the point of sale or care and the MGAs ready to integrate will capture that distribution. At the same time, digital-first customers now treat faster claims, self-service management, online policy access, and digital communication as the baseline, not the premium tier.

In the US pet insurance market, end-to-end digitisation is no longer a differentiator. For MGAs and the carriers backing them, it is becoming the price of entry.

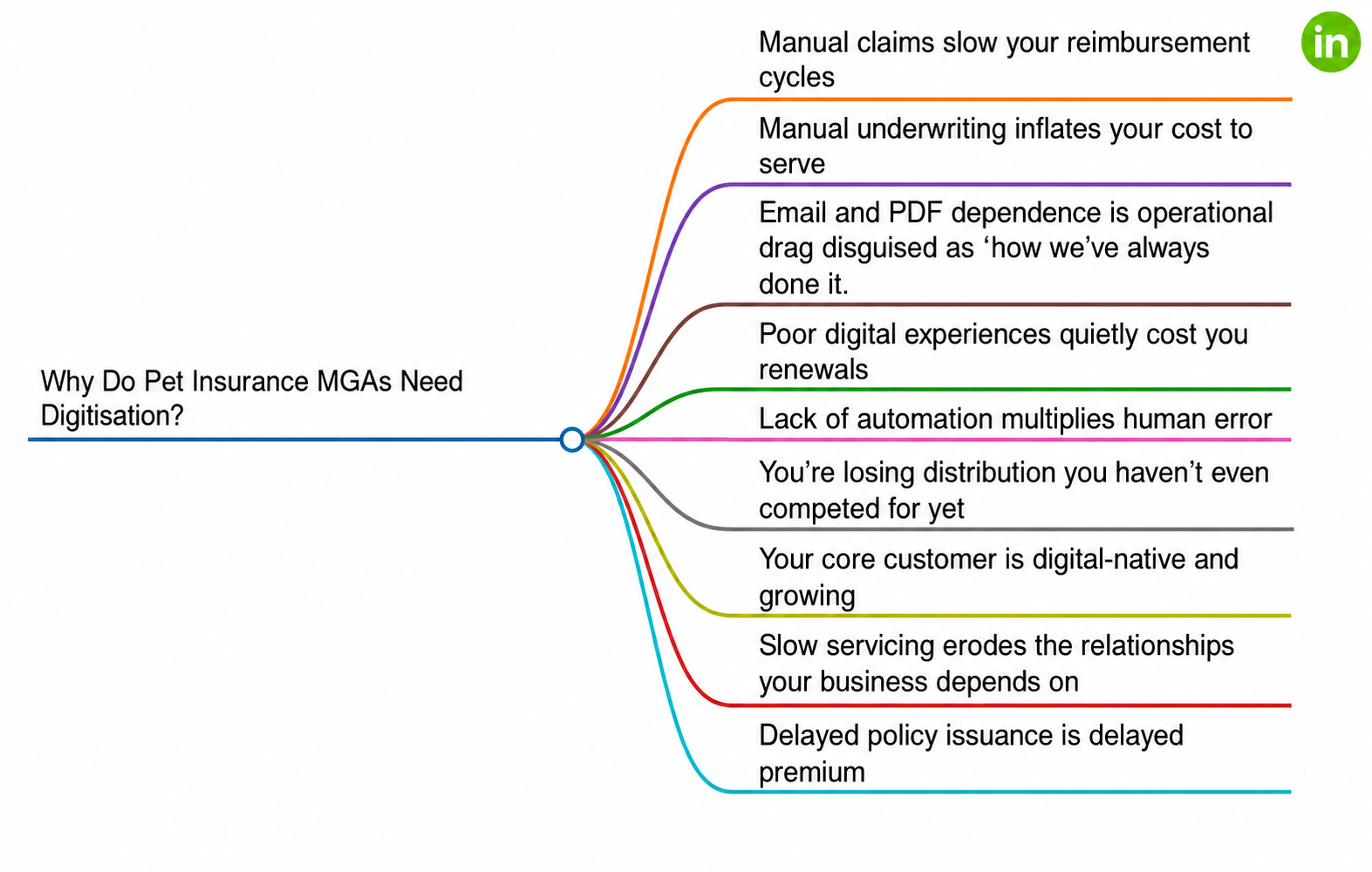

Why Do Pet Insurance MGAs Need Digitisation?

Pet insurance MGA digitisation is easy to defer. There's always a reason to wait another quarter. But for a pet insurance MGA, the cost of staying manual isn't theoretical it appears directly in your loss ratios, your retention curve, your partner relationships, and your premium growth. Here's where it hurts.

1. Manual claims slow your reimbursement cycles and reimbursement speed is retention

Every day a claim sits in an email queue is a day your customer questions whether the policy was worth it. Delayed claims processing is one of the quickest ways to erode satisfaction and trigger churn at renewal.

2. Manual underwriting inflates your cost to serve

When clear, decidable risks still require a human, you're paying underwriter time for work a rules engine should resolve in seconds. That cost scales linearly with volume which means growth makes the problem worse, not better.

3. Email and PDF dependence is operational drag disguised as "how we've always done it."

Re-keying data across disconnected tools creates delays, version-control chaos, and a back office that can't scale without adding people. It's invisible until you try to grow, and then it becomes the bottleneck holding you back.

4. Poor digital experiences quietly cost you renewals

Customers compare you not to other insurers, but to every smooth digital experience they encounter elsewhere. A clunky, manual journey reads as an untrustworthy one and retention suffers for reasons that never appear in an exit survey.

5. Lack of automation multiplies human error

Manual handoffs mean mis-keyed data, missed notifications, and inconsistent decisions each one a potential complaint, leakage point, or compliance exposure.

6. You're losing distribution you haven't even competed for yet

Embedded pet ecosystems are driving demand for API-based insurance infrastructure. If you can't integrate at the point of sale or care, that distribution simply flows to an MGA that can.

7. Your core customer is digital-native and growing

Millennials are the single largest group of pet owners at roughly 30%, with Gen Z close behind at around 21% together they account for over half the market. And Gen Z is the fastest-growing segment: in 2024 they made up about 20% of US pet-owning households (18.8 million), a 43.5% jump from the prior year (Source: American Pet Products Association, 2024 APPA National Pet Owners Survey), and they're the generation most likely to own multiple pets, with 70% owning two or more. Both generations expect digital pet insurance experiences as standard, not as a premium option. Gen Z in particular is mobile-first, research-driven, and quick to abandon any journey that feels clunky or paper-bound. Building for how the market used to buy means losing the two segments that are defining how it buys now.

8. Slow servicing erodes the relationships your business depends on

Brokers and partners direct volume to the MGAs that make their lives easy. Poor servicing doesn't just frustrate customers it quietly costs you partner loyalty and the referrals that come with it.

9. Delayed policy issuance is delayed premium

Every gap between quote and bind is revenue sitting idle and a window for the customer to leave. Issuance speed is premium growth, plainly stated.

The pattern is consistent: manual operations don't fail loudly. They bleed through slower cycles, higher costs, weaker retention, and lost distribution until a faster competitor makes the damage impossible to overlook.

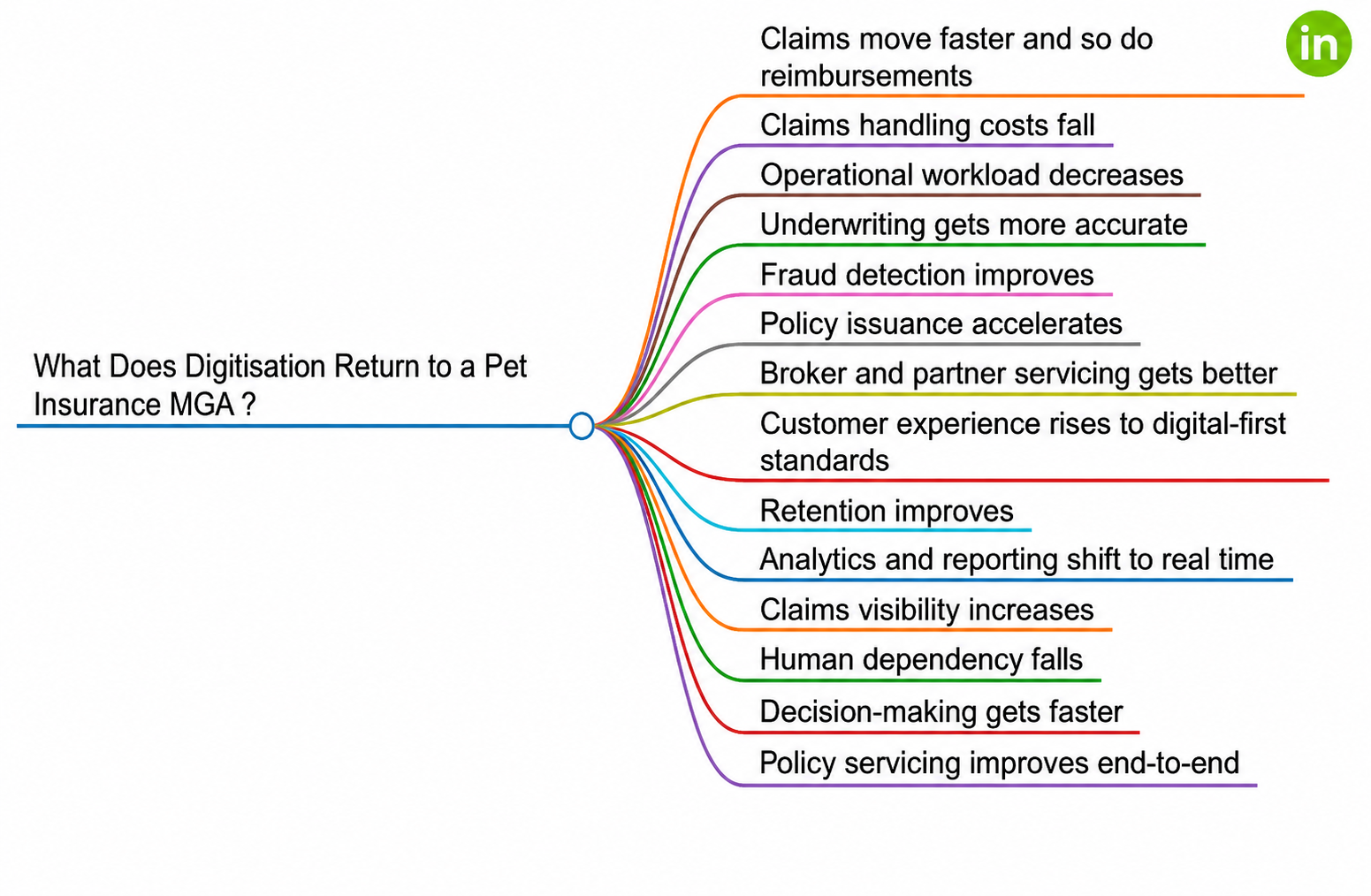

What Does Digitisation Return to a Pet Insurance MGA?

If the last section was the cost of standing still, this is the return on moving. Pet insurance MGA digitisation isn't a technology upgrade you justify on principle it's a set of measurable gains that show up across claims, underwriting, distribution, and the bottom line.

1. Claims move faster and so do reimbursements

Digital FNOL, automated triage, and AI-supported adjudication reduce cycle times from days to hours. Pet parents get reimbursed sooner, and faster reimbursement is the clearest signal that the policy was worth purchasing.

2. Claims handling costs fall

Automation removes the manual steps that make each claim costly to process. You handle greater volume without proportionally greater cost the economics finally shift in your favour as you scale.

3. Operational workload decreases

Connected workflows eliminate re-keying, chasing, and reconciling across emails and PDFs. The same team handles more business, and growth stops meaning additional headcount.

4. Underwriting gets more accurate

Data-driven STP (Straight-Through Processing, the automated binding of risks that meet predefined rules without human intervention) applies consistent rules to every clean risk, removing the variability of manual judgement. Decisions are faster and more defensible.

5. Fraud detection improves

Automated risk signals including pet-photo and pattern-based checks surface suspicious cases that manual review routinely misses, protecting your loss ratios.

6. Policy issuance accelerates

Automated, integrated issuance closes the gap between quote and bind. Less revenue sits idle, fewer customers drop off mid-journey, and premium recognises faster.

7. Broker and partner servicing gets better

Fast, frictionless servicing makes you the MGA partners want to send volume to turning distribution relationships into a compounding advantage.

8. Customer experience rises to digital-first standards

Self-service portals, digital communication, and online policy access meet customers where their expectations already sit.

9. Retention improves

Faster claims, smoother servicing, and a modern experience compound into the one metric that defines MGA value: customers who renew.

10. Analytics and reporting shift to real time

Cloud dashboards give you and your carriers live visibility into the book loss trends, claims status, and portfolio performance as they develop, not weeks later.

11. Claims visibility increases

Both your team and your customers can see exactly where a claim stands, reducing inbound queries and building trust.

12. Human dependency falls

Routine decisions run on rules and automation, freeing your people for the complex, judgement-heavy work that genuinely requires them.

13. Decision-making gets faster

Real-time data replaces month-end spreadsheets, so you act on what's happening now instead of what occurred last quarter.

14. Policy servicing improves end-to-end

From endorsements to renewals, every servicing interaction becomes faster, more consistent, and lower-cost.

The throughline: digitisation converts your operating model from a cost that grows with volume into a system that gets more efficient as you scale. That's the difference between an MGA that's hard to grow and one that's built to.

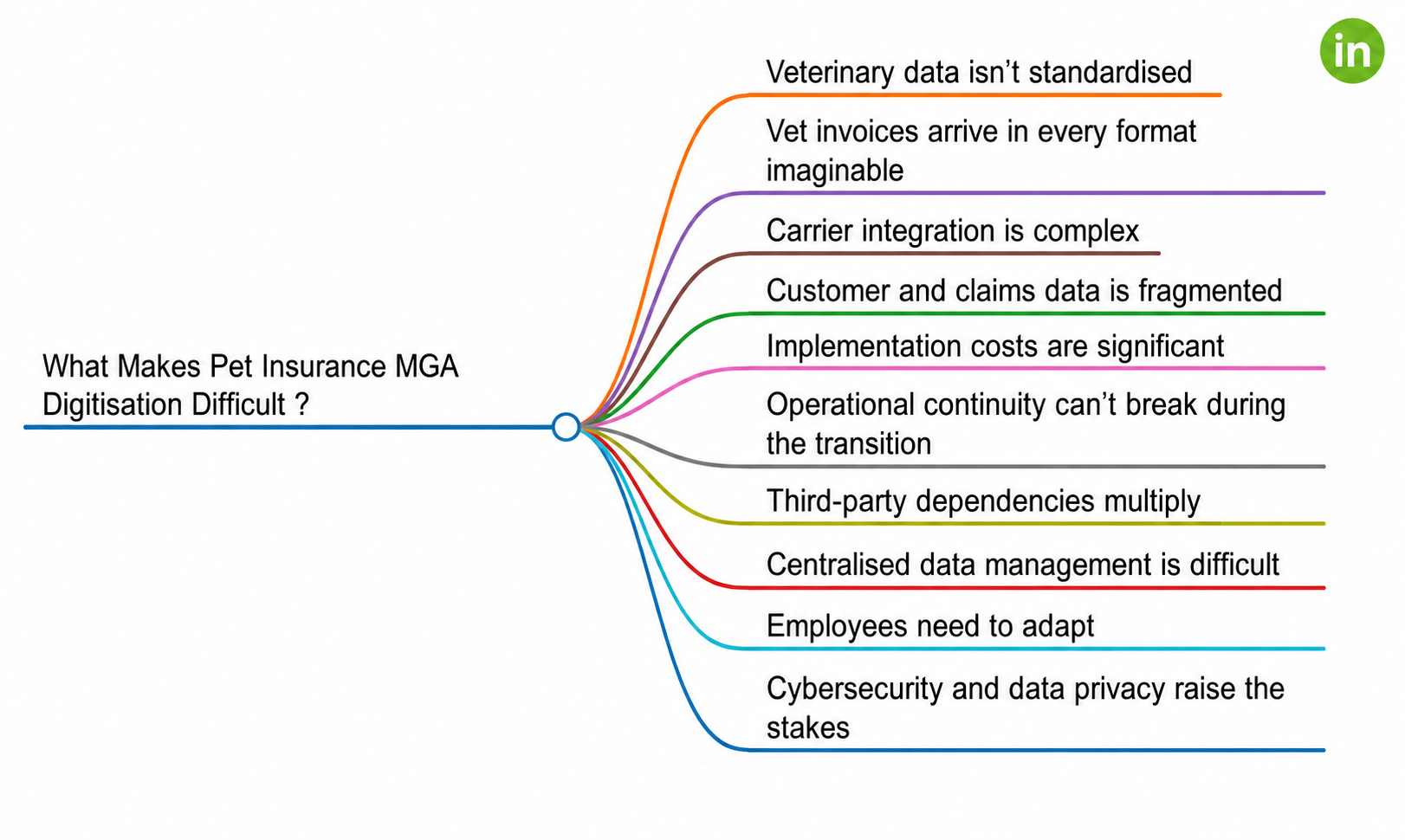

What Makes Pet Insurance MGA Digitisation Difficult?

None of this is to suggest pet insurance MGA digitisation is simple. It isn't and any MGA leader who's undertaken it knows the obstacles are real. Acknowledging them honestly matters, because the MGAs that succeed are the ones that plan for these challenges rather than encounter them mid-project.

1. Veterinary data isn't standardised

Unlike human health insurance, pet care has no universal coding standard. Diagnoses, procedures, and treatments are documented differently from clinic to clinic, which makes automated interpretation genuinely difficult.

2. Vet invoices arrive in every format imaginable

Handwritten notes, scanned PDFs, clinic-specific templates, itemised printouts there is no common structure. Building automation that reads them reliably is a real engineering challenge, not a plug-in.

3. Carrier integration is complex

Every carrier brings its own APIs, data requirements, and workflows. Connecting cleanly to multiple carriers each with different standards is one of the heaviest undertakings in any MGA digitisation effort.

4. Customer and claims data is fragmented

Information typically sits scattered across spreadsheets, email threads, partner systems, and legacy tools. Consolidating it into a single reliable source is a prerequisite for automation and often the most demanding groundwork.

5. Implementation costs are significant

Building or integrating modern infrastructure requires real upfront investment in technology, integration, and change management. The return is strong, but the initial outlay is a genuine consideration.

6. Operational continuity can't break during the transition

The business has to keep quoting, binding, and paying claims while it transforms underneath. Migrating without disrupting live operations requires careful sequencing.

7. Third-party dependencies multiply

Modern MGA stacks rely on multiple external systems payment providers, communication channels, data sources, carrier platforms. Each dependency adds integration and reliability risk that needs to be managed.

8. Centralised data management is difficult

Pulling fragmented data into one governed, accessible, real-time system is a substantial undertaking and the foundation everything else depends on.

9. Employees need to adapt

New systems mean new workflows. Without proper training and change management, adoption stalls and the investment underdelivers the technology is rarely the hard part; the people transition is.

10. Cybersecurity and data privacy raise the stakes

Digitising means handling sensitive customer and payment data at scale, which brings real obligations around security, compliance, and privacy non-negotiable in the US regulatory environment.

The takeaway isn't that these challenges should slow you down it's that they should shape how you sequence the work. The MGAs that succeed don't sidestep these issues; they choose a partner and an approach built to address them from the start.

How Do You Digitise a Pet Insurance MGA End-to-End?

Knowing why pet insurance MGA digitisation matters is the easy part. The real question for any MGA leader is how what actually gets built, and in what shape. End-to-end digitisation breaks down into five connected workstreams. Each delivers value on its own, and together they form the complete digital MGA.

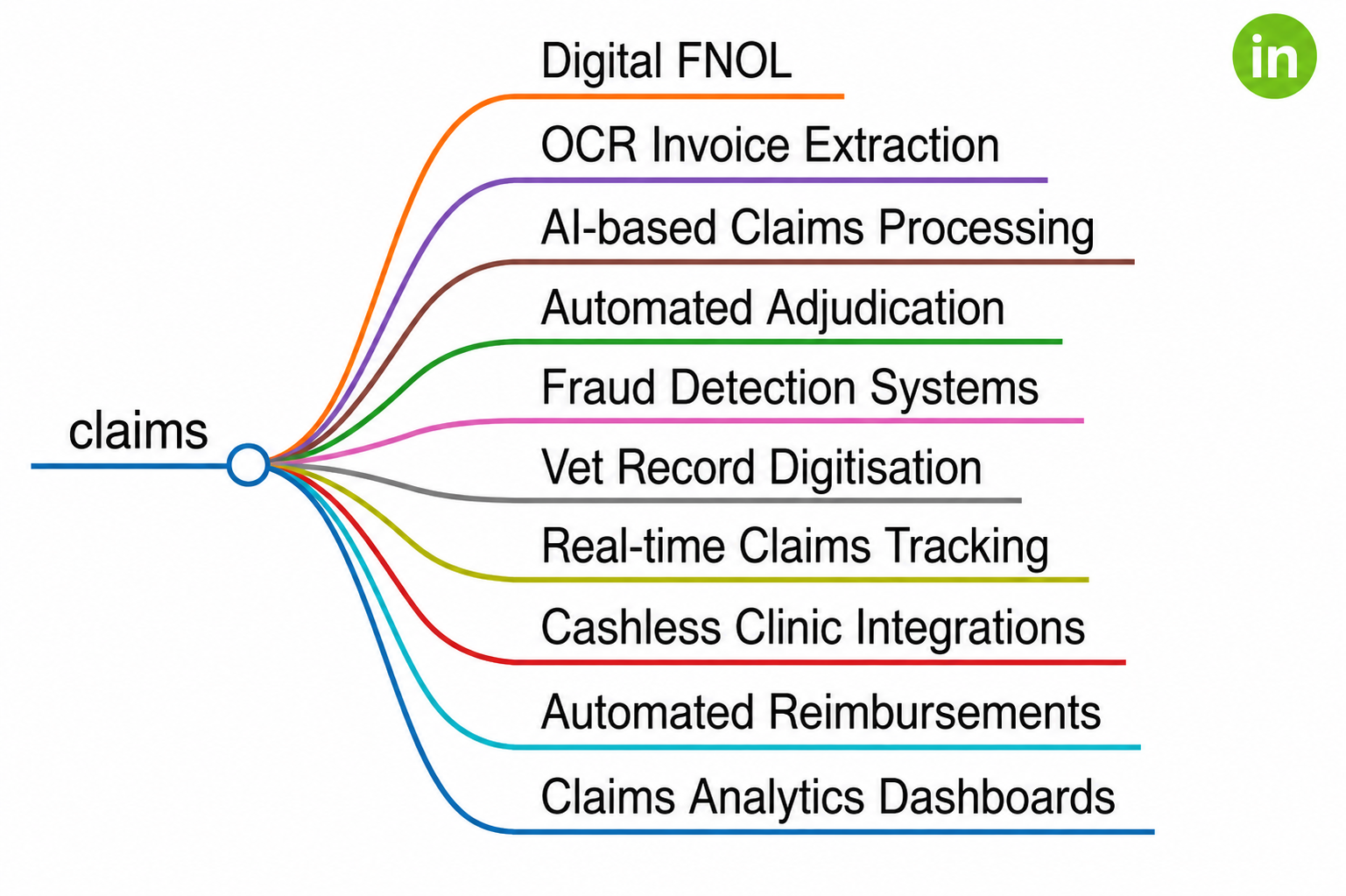

1. Claims the workstream that defines your reputation

This is where speed and accuracy convert directly into retention, so it's where most of the operational complexity lives.

A. How does digital FNOL work for pet insurance claims?

Digital FNOL (First Notice of Loss) lets pet parents file a claim from their phone in minutes upload invoices, describe the incident, and submit without a phone call or paperwork. That first interaction sets the tone for the entire claim.

B. What is OCR invoice extraction in pet insurance?

OCR (Optical Character Recognition) invoice extraction is purpose-built technology that reads vet invoices in any format, handwritten, scanned, or digitally generated, and converts them into structured, usable data. This is the foundation that makes automated claims processing possible.

C. How does AI-based claims processing work for pet insurance?

AI-based claims processing uses intelligent triage that classifies, validates, and routes each claim automatically, sending clean cases down a fast lane and flagging the rest for human review.

D. What is automated adjudication in pet insurance claims?

Automated adjudication is rules-based decisioning that settles straightforward claims instantly against policy terms, cutting cycle times from days to hours without any human intervention.

E. How does fraud detection work in pet insurance claims?

Automated screening scores every claim for risk signals before payout, protecting loss ratios without slowing legitimate claims. Pattern-based checks surface suspicious behaviour invisible to case-by-case review.

F. What is vet record digitisation?

Vet record digitisation converts unstructured clinical records and medical histories into searchable, structured data that supports faster, more accurate underwriting and claims decisions.

G. How does real-time claims tracking benefit pet insurance customers?

Real-time claims tracking gives customers and staff a live status view of every open claim, eliminating the "where's my claim?" support calls that clog queues and damage trust.

H. What is cashless clinic settlement in pet insurance?

Cashless clinic integration means direct settlement to partner vet clinics so pet parents never pay out of pocket the single most differentiated claims experience a pet insurance MGA can offer.

I. How do automated reimbursements work?

Automated reimbursements are straight-through payouts to customers once a claim is approved, with no manual finance step in between enabling same-day or next-day settlement.

J. What do claims analytics dashboards track?

Claims analytics dashboards provide live visibility into cycle times, leakage rates, fraud scores, and loss trends so leadership manages the book on real data, not month-end reports.

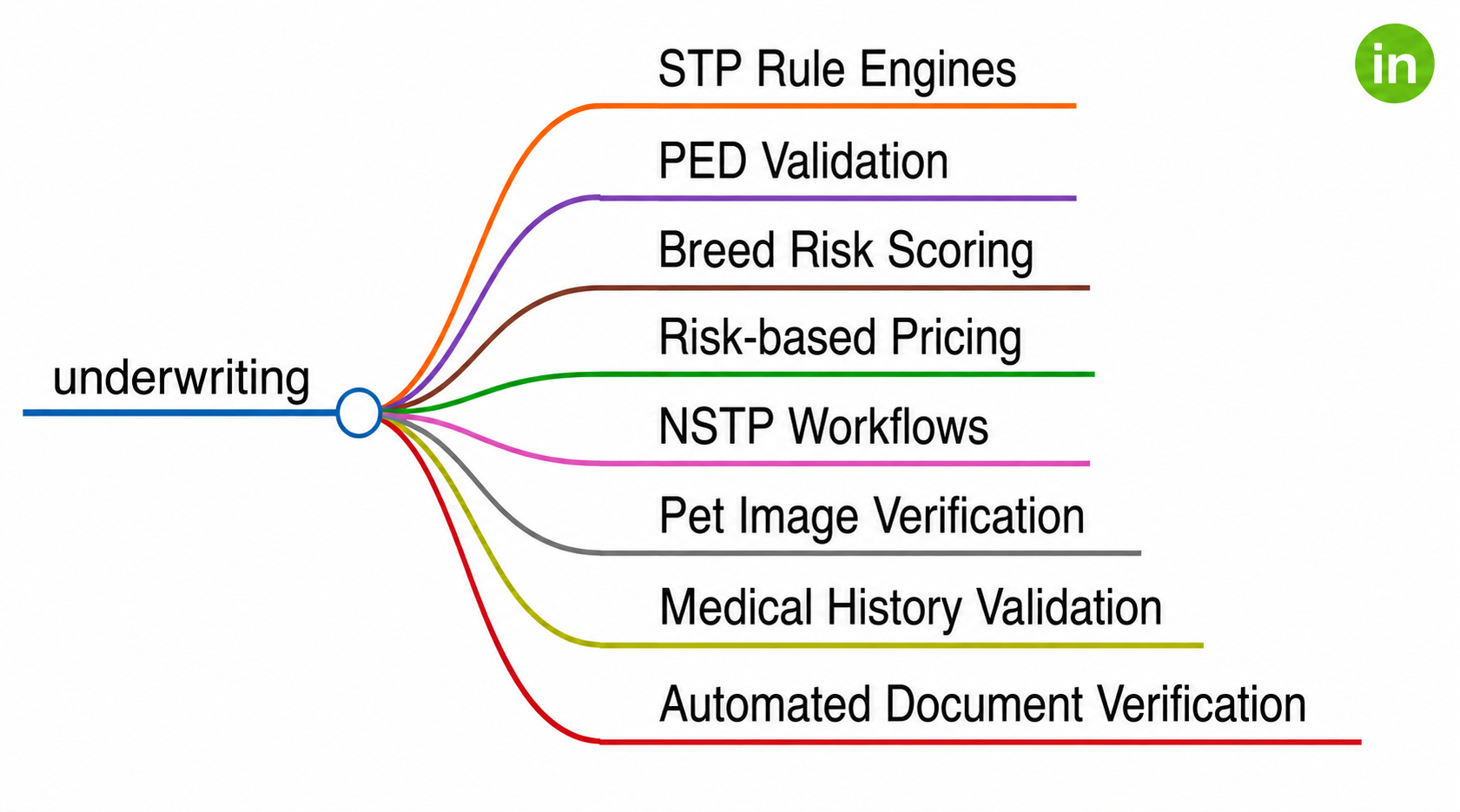

2. Underwriting the engine for scaling volume profitably

The goal is clear: decide clean risks instantly and route only the complex ones to humans.

A. What is straight-through processing (STP) in pet insurance underwriting?

Straight-through processing (STP) is automated underwriting that binds clean risks in seconds using structured data age, breed, location, pre-existing condition status with no underwriter involvement required. It's how MGAs grow submission volume without growing the underwriting team.

B. What is PED validation in pet insurance underwriting?

PED (Pre-Existing Disease) validation runs automated checks against medical history for every application, applied consistently rather than relying on individual underwriter judgement.

C. How does breed risk scoring affect pet insurance pricing?

Breed risk scoring uses data-driven models to price breed-specific risk accurately accounting for hereditary conditions, size-related claims frequencies, and regional prevalence rather than relying on broad assumptions.

D. What is risk-based pricing in pet insurance?

Risk-based pricing reflects actual exposure across age, breed, location, and selected cover level protecting MGA margins while remaining competitive on the policies worth winning.

E. What are NSTP workflows in pet insurance?

NSTP (Non-Straight-Through Processing) workflows are structured referral paths that route complex underwriting cases to the right underwriter with all relevant context already attached, eliminating manual triage.

F. How does pet image verification work in underwriting?

Pet image verification uses photo-based AI checks to confirm the pet's identity, assess visible health conditions, and flag risk or fraud signals at the point of underwriting before a policy is issued.

G. What is medical history validation in pet insurance?

Medical history validation is automated cross-referencing of declared health history against available veterinary records to identify gaps, inconsistencies, or undisclosed pre-existing conditions.

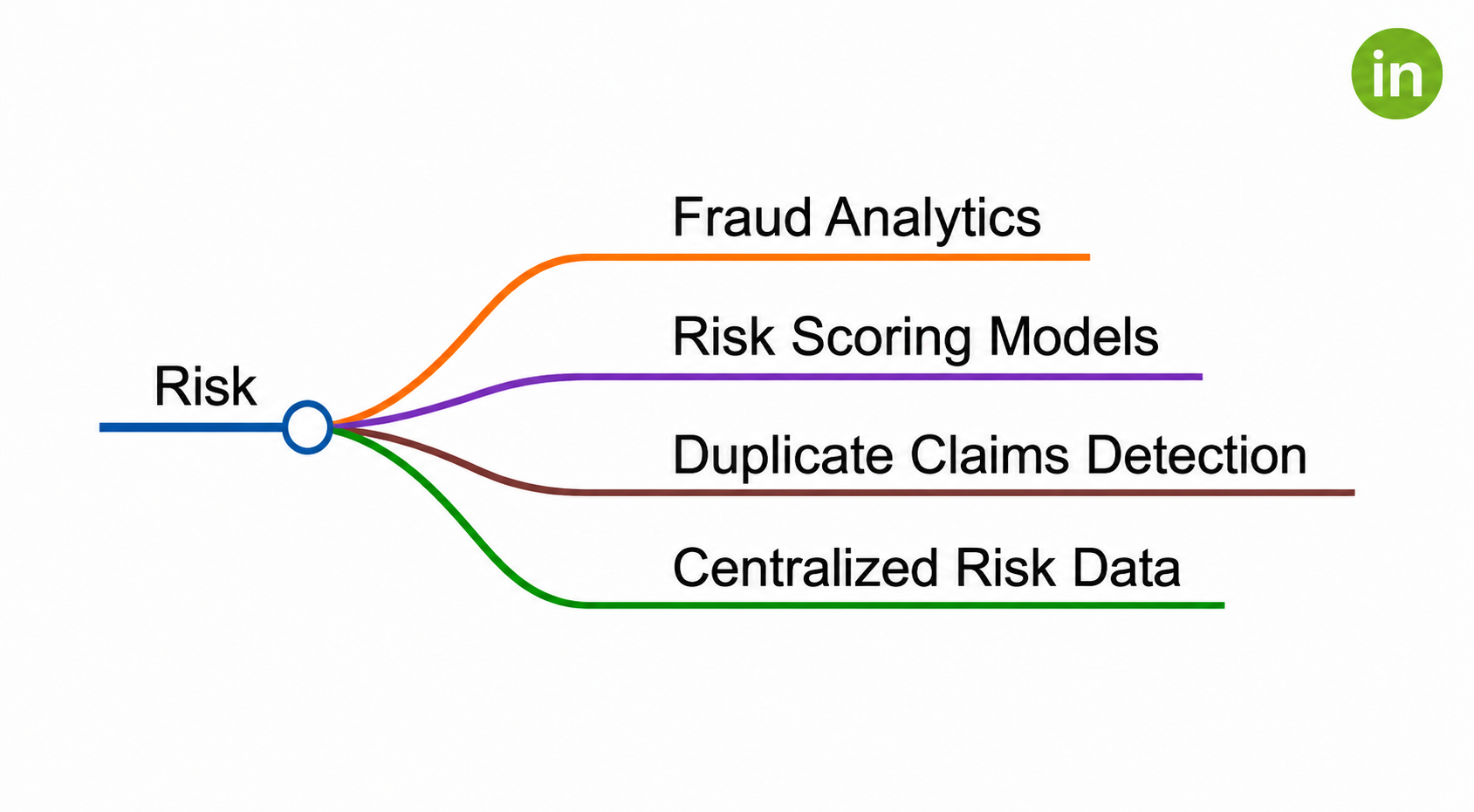

3. Risk the layer that protects your loss ratios

Running across claims and underwriting sits a dedicated risk function that keeps the whole book healthy.

A. What is fraud analytics in pet insurance?

Fraud analytics is pattern detection across claims populations and customer behaviour that surfaces organised or repeat fraud invisible to individual case-by-case review.

B. How does duplicate claims detection work?

Duplicate claims detection uses automated matching to identify the same invoice or incident submitted more than once a common and costly source of claims leakage in pet insurance portfolios.

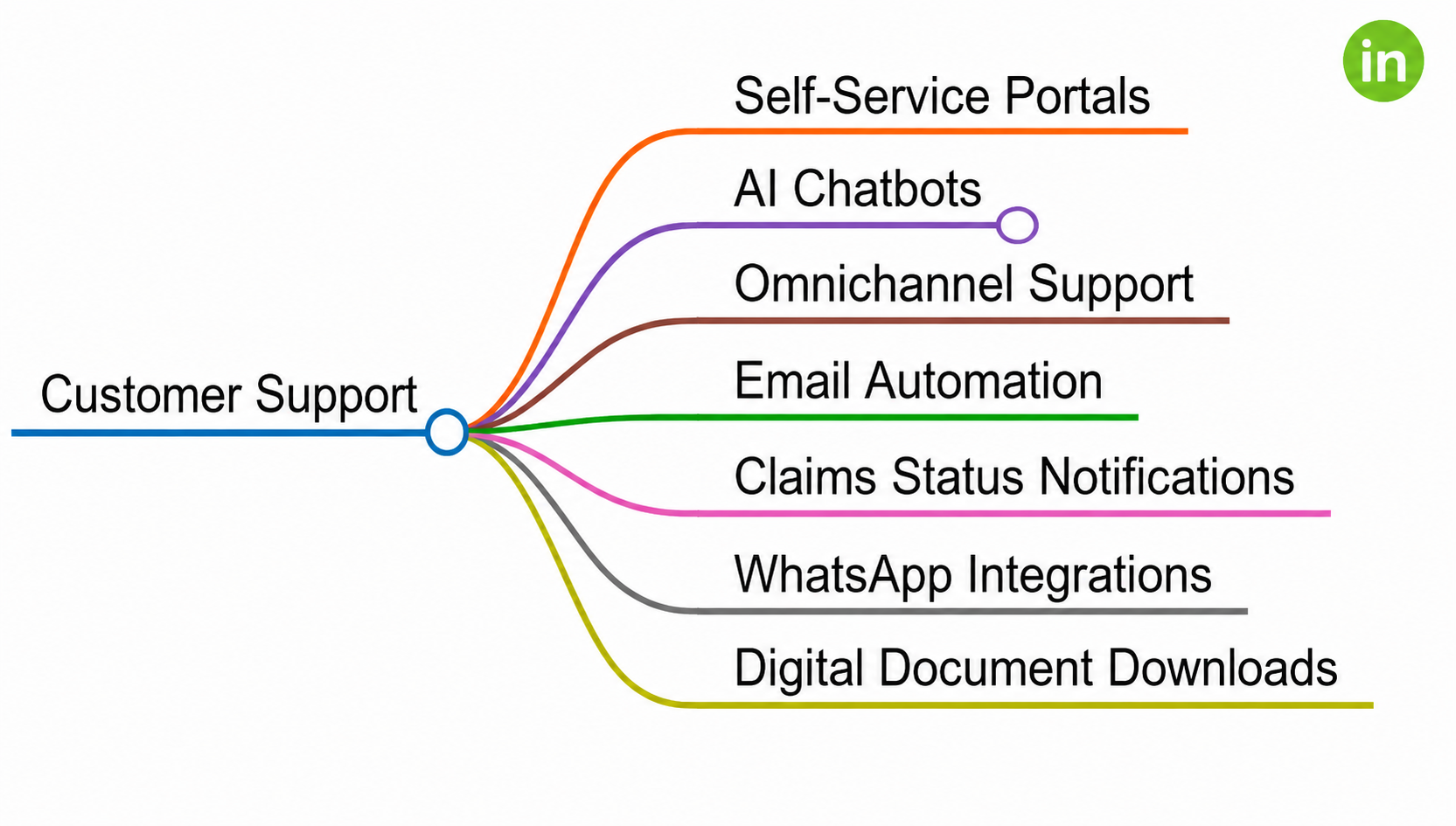

4. Customer support self-service as the default, humans for the exceptions

A modern support stack resolves routine requests instantly and reserves people for what genuinely needs them.

A. What should a pet insurance self-service portal include?

A pet insurance self-service portal should let customers view their policy, file and track claims, manage renewals, update personal details, and access digital documents without contacting anyone on the MGA's team.

B. How do AI chatbots reduce support costs for pet insurance MGAs?

AI chatbots provide instant answers to common questions around the clock, deflecting routine queries before they reach a human agent. This lowers cost per contact while improving response speed for customers.

C. What is omnichannel support in pet insurance?

Omnichannel support means a connected service experience across chat, call, email, and messaging platforms so customers never need to repeat their situation when moving from one channel to another.

5. Distribution capturing demand wherever it forms

This is how the MGA grows reach without growing friction.

A. What is embedded insurance in the pet ecosystem?

Embedded insurance means coverage offered natively inside pet e-commerce checkouts, veterinary telehealth flows, grooming bookings, and partner platforms at the natural point of purchase or care, rather than requiring the customer to seek out a policy separately.

B. How do API-based partner integrations work for pet insurance MGAs?

API-based partner integrations provide clean, documented interfaces that let vet clinics, pet retailers, and ecosystem partners connect quickly and begin distributing coverage without custom development on their end.

C. What is a broker and agency portal for pet insurance?

A broker and agency portal is a dedicated digital tool that makes it fast and easy for intermediaries to quote, bind, and service pet insurance business without calling or emailing the MGA for each transaction.

The architecture matters as much as the individual components. These workstreams shouldn't be five separate tools bolted together they should share data, communicate with each other, and operate as one connected system. That integration is what turns a collection of features into a genuine end-to-end platform and it's the difference between digitising tasks and digitising the business.

Conclusion

The US pet insurance market is being reshaped by embedded ecosystems and digital-first owners faster than most operating models can keep up. For MGAs, pet insurance MGA digitisation has shifted from competitive edge to table stakes the foundation that carriers reward, partners prefer, and customers now expect by default.

The challenges are real, but they're solvable with the right sequencing and the right partner. The opportunity is larger: an operating model that gets more efficient as it scales, instead of more expensive. That's the MGA worth building.

Frequently Asked Questions

What does end-to-end digitisation mean for a pet insurance MGA?

End-to-end digitisation for a pet insurance MGA means automating the complete policy lifecycle from API-driven quoting and STP underwriting through digital claims adjudication and self-service renewals so that the business scales volume without scaling headcount or manual operational cost.

How does automated underwriting reduce costs for a pet insurance MGA?

Automated underwriting applies consistent rules to every clean risk and binds decisions in seconds without underwriter involvement. This removes the linear cost relationship between submission volume and team size, meaning each additional policy costs progressively less to underwrite as volume grows.

What is straight-through processing (STP) in pet insurance?

Straight-through processing (STP) is automated binding of insurance applications that meet predefined eligibility rules without any human review. In pet insurance, STP handles cases where breed, age, location, and declared health history all fall within acceptable parameters typically the majority of incoming applications.

Why is claims speed important for pet insurance MGA retention?

Claims speed is the primary moment customers evaluate whether their policy was worth buying. Delayed reimbursements signal unreliability and directly increase churn at renewal. Faster claims enabled by digital FNOL, OCR invoice reading, and automated adjudication are the single highest-return investment a pet insurance MGA can make in customer lifetime value.

What is embedded insurance in the context of the pet ecosystem?

Embedded insurance in the pet ecosystem means coverage offered natively inside non-insurance platforms vet clinic booking systems, pet e-commerce checkouts, telehealth apps, or microchip registrations at the moment the customer is already engaged with their pet's health or care. This captures demand before the customer ever searches for a standalone policy.

What are the biggest challenges in digitising a pet insurance MGA?

The main challenges are: lack of standardised veterinary data and invoice formats, complexity of integrating with multiple carriers on different API standards, fragmented customer and claims data sitting across legacy tools, the cost of implementation, and maintaining business continuity during the transition. Each is solvable with the right sequencing and technology partner.

What technology does a modern pet insurance MGA platform need?

A modern pet insurance MGA platform needs: an API-driven quote-to-bind engine, STP underwriting rules engine, OCR-based invoice extraction, AI claims adjudication, fraud scoring models, a customer self-service portal, omnichannel support stack, broker and agency portal, and real-time analytics dashboards all sharing a single data layer rather than operating as disconnected tools.

How does cashless vet clinic settlement work in pet insurance?

Cashless settlement means the MGA pays the vet clinic directly on approved claims, so the pet owner never pays out of pocket and seeks reimbursement later. It requires pre-integration between the MGA's claims platform and the clinic's billing system, and is the most differentiated claims experience a pet MGA can offer in the US market today.