Pet Insurance Claims Financing: Why Defaults Stay High

The Hidden Data Gap Behind Every Pet Insurance Claims Financing Default

Pet insurance claims financing is a bridge lending model where a financing company advances funds to a pet owner at the point of veterinary care before the insurer has reviewed or approved the claim and is repaid once the insurance reimbursement arrives. Because US pet insurance runs on reimbursement rather than direct billing, the owner pays the vet upfront and waits to be paid back, and pet insurance claims financing fills that gap. Understanding the average pet insurance claim settlement cycle is critical to modeling the economics of this bridge. The problem most lenders face is that they underwrite these loans without real-time coverage data, which is why their default rates stay higher than the borrower base should produce.

This article explains how pet insurance claims financing works, why the reimbursement model creates structural risk for lenders, what it costs across the P&L, and the infrastructure that resolves it.

What Is Pet Insurance Claims Financing?

Pet insurance claims financing is a bridge lending arrangement in which a financing company fronts money to a pet owner at the point of veterinary care, before the insurer has reviewed or approved the claim. The owner repays that advance once the reimbursement comes through.

The model exists because US pet insurance runs almost entirely on reimbursement. A well-designed end-to-end claims workflow shortens that reimbursement cycle, but most MGAs and financing providers still operate without one. Unlike human health insurance, there is no direct billing between vets and insurers. The owner pays the clinic upfront, files a claim, and then waits sometimes for weeks to be paid back. Emergency surgeries commonly land between $3,000 and $10,000, and most American households do not keep that kind of money liquid.

Pet insurance claims financing closes that gap. But closing it is far harder than it first appears.

Why the US Pet Insurance Reimbursement Model Creates a Financing Problem

Reimbursement was built for an earlier era, when pet insurance was a niche product serving a financially comfortable slice of the market. That has changed. NAPHIA data now shows more than 6 million pets insured in the US, climbing at double-digit rates year over year. The customer base has widened considerably. So has the size of the average emergency claim, driven by veterinary cost inflation, advanced diagnostics, specialty surgery, and oncology care that did not even exist a decade ago.

Each dollar of veterinary inflation pushes up the average loan a financing company has to write. And each dollar advanced against an unverified, unconfirmed claim raises the odds that the loan repays late, or never.

In effect, the financing company is absorbing the structural inefficiency of the reimbursement model. The real question is how to stop absorbing it and start managing it.

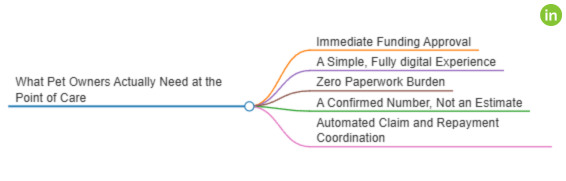

What Pet Owners Actually Need at the Point of Care

To understand why the current pet insurance claims financing experience falls short and what fixing it demands you have to start with the borrower's situation.

A pet owner standing in an emergency clinic is not making a calm financial choice. They are in crisis. Their animal is in pain. The vet is waiting on financial authorization before treating. The decision gets made in under five minutes, under intense emotional pressure, with incomplete information.

That reality produces five specific needs, most of which today's products meet only halfway:

1. Immediate funding approval

Treatment will not wait. A 24-hour review, a document-upload requirement, or a verification callback has no place in emergency care. Approval has to happen at the clinic, in real time.

2. A simple, fully digital experience

Owners expect to apply on a phone, get an instant answer, and sign electronically. Any step that demands a paper form, a phone call, or a separate portal breaks the flow at the worst possible moment.

3. Zero paperwork burden

An owner who has just learned their dog needs emergency surgery is not about to dig out policy documents, hunt for an insurance ID card, or call their insurer to confirm coverage. The workflow has to handle all of that automatically, on their behalf.

4. A confirmed number, not an estimate

"We think you're probably covered up to roughly this amount" is not a usable answer when the alternative is declining surgery. The owner needs a firm, confirmed financing figure before authorizing treatment.

5. Automated claim and repayment coordination

Once they leave the clinic, the owner's focus is on their animal's recovery. They expect claim submission, reimbursement tracking, and loan repayment to run as one coordinated, automated process not as three separate tasks to juggle manually while emotionally drained.

The market consistently fails on the last three. That failure is what drives abandonment, customer complaints, and needless operational load.

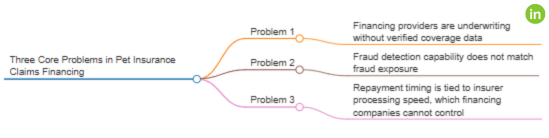

The Three Core Problems in Pet Insurance Claims Financing

Problem 1: Financing providers are underwriting without verified coverage data

What happens: A financing company approves a bridge loan based on what the owner says about their policy with no real-time check on whether the policy is active, whether the procedure is covered, whether the annual limit is spent, or where the deductible stands. Automated underwriting solves this on the carrier side, but financing providers rarely have access to the same data.

Why it happens: Pet insurers don't currently expose real-time policy verification APIs for outside use. No standard mechanism exists for a financing provider to query coverage at the point of care. Where verification occurs at all, it's manual a call to the insurer that eats time the emergency does not allow.

What it costs: Loans approved against policies that don't cover the procedure, that have already hit their annual cap, or that carry pre-existing-condition exclusions the owner never knew about all turn into elevated default risk. The financing company ends up pricing a portfolio of unknowns rather than a portfolio of verified coverage.

Problem 2: Fraud detection capability does not match fraud exposure

What happens: Veterinary invoices arrive in non-standard formats from dozens of different practice management systems. Doctored invoices, padded line items, fabricated procedure codes, and the same claim submitted to several financing providers at once are all structurally hard to detect. A purpose-built claims fraud detection framework catches most of these patterns but few financing companies have one.

Why it happens: There is no standard veterinary billing code set equivalent to the CPT codes used in human healthcare. Every PMS Avimark, Cornerstone, ezyVet, Shepherd, ImproMed formats invoices its own way. No clearinghouse audits claims before they reach the financing company. Detection leans on manual review and rule-based checks that neither scale nor catch sophisticated manipulation.

What it costs: Fraud losses individually small enough to dismiss as portfolio variance, yet collectively large enough to materially squeeze margins. And because the fraud is so hard to spot, the true loss is always higher than the booked figure.

Problem 3: Repayment timing is tied to insurer processing speed, which financing companies cannot control

What happens: A bridge loan built on a 30-to-60-day repayment assumption stretches into a 90-day-plus position when insurer processing slows, when a claim triggers secondary review, or when extra documentation gets requested.

Why it happens: Insurer processing timelines vary by 3x or more across the market understanding carrier claims payment speed is essential to modeling repayment risk. Many carriers still run legacy administration systems that settle in batch cycles. There is no real-time claim-status visibility for the financing company after approval. You find out repayment will be late when the loan goes past due.

What it costs: Capital trapped in extended positions that can't recycle into new loans. Collections actions against accounts that are delinquent because of timing mismatches, not customer bad faith. Damaged relationships and inflated cost-to-collect on loans that will, in the end, repay.

What This Costs a Pet Insurance Financing Company By Line Item

The damage from these three problems doesn't stay contained. It spreads across the P&L all at once.

1. Elevated loan default rates

Default rates run higher than the borrower base's underlying credit quality would predict. Building accurate claims reserve estimation methods becomes almost impossible when the input data is this noisy. Insured owners with legitimate claims in process are not inherently high-risk. But unverified coverage, partial reimbursements, and processing delays convert low-risk borrowers into delinquent accounts. The root cause is missing underwriting data, not borrower quality.

2. High operational and verification costs

Every loan you can't verify electronically requires manual insurer outreach calls, IVR navigation, hold times, follow-ups. At scale, it becomes one of the heaviest per-loan cost items in the operation. It's also almost entirely automatable with the right infrastructure.

3. Delayed repayments compressing cash flow

Capital locked in stretched bridge positions can't be redeployed. When settlement takes 90 days instead of 45, the financing company either sits on excess reserve capital or constrains new loan volume. Both carry a direct cost.

4. Fraud-related financial losses

Without intelligent document processing, fraud clears at a rate manual review can't match. The losses are real, they grow with loan volume, and they're systematically underestimated because detection capability doesn't keep pace with exposure.

5. Heavy manual verification workload

The operations team spends significant hours each week on verification tasks that shouldn't need a human at all. That time carries an opportunity cost it's capacity not spent on exception handling, risk analysis, or product development.

6. High customer recovery and collections cost

Collecting on bridge loans where the delinquency comes from insurer processing delays rather than customer bad faith is expensive and relationship-damaging. On smaller loans, recovery cost frequently approaches or exceeds the outstanding balance.

7. Reduced profitability margins

All of the above compresses margins from several directions simultaneously. Risk pricing has to absorb coverage uncertainty. Operational cost inflates cost-per-loan. Collections eat into net recovery. The result is a business straining harder than it should for the returns it generates.

The combined effect is recoverable. But recovering it takes infrastructure, not operational effort.

Why the Current System Cannot Fix Itself

The problems above aren't operational failures that better processes will resolve. They're structural—rooted in technology gaps, data gaps, and integration gaps that run through the entire pet insurance claims financing ecosystem.

1. Legacy insurer systems were not built for real-time external verification

Most carrier policy administration platforms the core technology systems that run day-to-day operations were designed for a world where verification happened by phone or mail over several days. Even insurers who want to support real-time verification often can't easily expose that capability through APIs an outside party can safely query. At most carriers, the integration infrastructure simply isn't there.

2. There is no standardized veterinary data layer

Human healthcare has CPT codes, HL7, FHIR, and a clearinghouse infrastructure that normalizes billing data across thousands of providers. Pet healthcare has none of it. Every clinic, every PMS, every invoice is different. There is no pet-health EHR equivalent—no central data model pulling a pet's medical history, prior claims, and treatment records into a queryable format. Without that layer, every claim is underwritten in isolation, stripped of the context that would make fraud detection and risk assessment meaningfully sharper.

3. The three-party integration problem has no natural owner

The vet clinic, the insurer, and the financing company are three separate parties with separate systems, separate incentives, and no shared infrastructure. The PMS doesn't connect to the insurer. The insurer doesn't connect to the financing company. The financing company can't close the repayment loop automatically. Every handoff among the three is manual—and manual handoffs are exactly where friction, errors, and fraud opportunities concentrate.

4. API ecosystem connectivity is immature

Even where integrations are technically feasible, they largely haven't been built. The business case for each party to invest in integration hasn't historically been strong enough—but that is shifting as market scale grows and the cost of the current model becomes harder to absorb.

How Tech and AI Solves the Pet Insurance Claims Financing Problem

The technology to address each structural gap already exists. The missing piece has been the orchestration layer that connects it to the financing workflow.

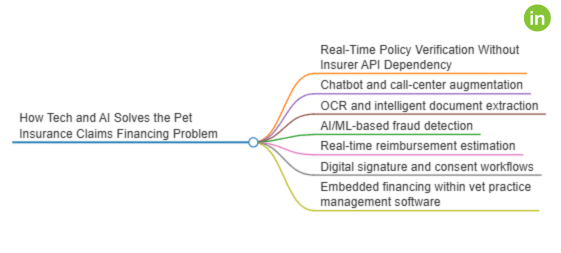

1. Real-Time Policy Verification Without Insurer API Dependency

The insurer grants the financing company read-only access to a dedicated email account used solely for sending policy details to policyholders. When an owner applies for financing, the company uses the submitted policy details to locate the matching policy email and extracts the coverage information through OCR and AI-based document extraction confirming instantly whether the policy is genuine, active, and covers the pet, with no manual verification call and no insurer API dependency.

2. Chatbot and Call-Center Augmentation

For carriers without API access, or for edge cases that need human judgment, AI-powered chatbots like a pet coverage Q&A chatbot handle the first round of insurer outreach, work through IVR systems, and escalate to a human agent only when the automated path stalls. Automation absorbs the volume; people handle the exceptions; per-loan verification cost falls significantly.

3. OCR and Intelligent Document Extraction

Veterinary invoices in any format any PMS, any layout—are ingested and converted into standardized structured data. Procedure codes are extracted and validated. Line items are cross-checked against geographic pricing benchmarks using vet fee schedule benchmarking. Document integrity is tested for manipulation signatures: altered metadata, font inconsistencies, mismatched totals. A document that once required manual review is processed, structured, and fraud-scored in seconds.

4. AI/ML-Based Fraud Detection

Machine learning models work at the portfolio level cross-referencing invoices across financing providers, flagging procedure codes that don't match the stated diagnosis, surfacing clinic-level patterns that signal systematic manipulation through organized fraud ring detection. The fraud signal sharpens over time as the model sees more data. Manual review teams can't replicate this structurally.

5. Real-Time Reimbursement Estimation

By combining verified coverage data, extracted procedure codes, and historical insurer settlement data by procedure type and carrier, the estimation engine—powered by claim settlement calculation logic produces a specific reimbursement probability with a confidence range before the financing decision is made. Not an approximation. A defensible number that informs the credit decision and gives the owner the confidence to authorize treatment.

6. Digital Signature and Consent Workflows

A single digital consent at the point of care covers the financing authorization, the claim-submission assignment, and the repayment trigger. No paper. No follow-up portal. No separate call. Fully documented and legally compliant—completed in under a minute at the clinic.

7. Embedded Financing Within Vet Practice Management Software

This is the solution that collapses the repayment-timing problem entirely. When financing origination, claim submission, and repayment triggering are orchestrated as one workflow inside the vet's PMS built on an API-first insurance platform repayment fires automatically the moment the insurer settles. Capital recycles on a defined, predictable timeline not dependent on customer behavior or outbound collections.

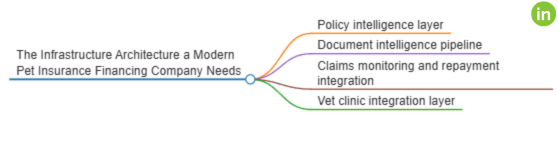

The Infrastructure Architecture a Modern Pet Insurance Financing Company Needs

Solving pet insurance claims financing at scale is not a single product. It is four connected layers:

Policy intelligence layer - real-time coverage verification through API, email automation, and document parsing, feeding a [treatment cost estimation](/agents/treatment-cost-estimation-ai-agent-in-claims-for-pet-insurance engine that informs every credit decision before approval.

Document intelligence pipeline - OCR and LLM-based invoice extraction, fraud scoring, procedure-code validation, and standardized structured output for every veterinary invoice, regardless of source system or format.

Claims monitoring and repayment integration - post-approval claims cycle time analytics, settlement-notification intake from insurers, and automated repayment triggering on settlement. No manual collections on standard claims.

Vet clinic integration layer - embedded within practice management software or delivered through a clinic-facing application, turning financing application, digital consent, and claim submission into a single connected point-of-care experience.

The choice is whether to build, acquire, or partner starting with the right banking and financial infrastructure. What is not a viable option is continuing to operate without it as the market matures.

The Competitive Window

The pet insurance claims financing market is growing. Veterinary cost inflation keeps lifting average loan sizes. Institutional capital is paying closer attention to the sector. And the infrastructure gap between leading and lagging financing providers is beginning to produce measurable differences in unit economics. The advantage goes to whoever closes the data gap first.

Frequently Asked Questions

What is pet insurance claims financing?

Pet insurance claims financing is a bridge lending model where a financing company advances funds to a pet owner at the point of veterinary care, before the insurer has approved the claim, and is repaid once the insurance reimbursement arrives. It exists because US pet insurance is reimbursement-based, meaning owners must pay the vet upfront and wait to be reimbursed.

What is the main risk for pet insurance financing companies in the US?

The primary risk is extending credit against insurance coverage that hasn't been verified in real time. Without confirming that the policy is active, the procedure is covered, and the annual limit is available, financing companies price a portfolio of unknowns which produces default rates above what the underlying borrower quality would justify.

Why is pet insurance claims fraud difficult to detect?

Because veterinary invoices have no standard format and no industry clearinghouse audits claims before they reach financing providers. Every practice management system formats invoices differently, which makes automated anomaly detection hard without purpose-built OCR and machine learning tooling.

How does embedded financing reduce default risk in pet insurance?

By fusing financing origination, claim submission, and repayment triggering into a single automated workflow. When repayment is triggered by insurer settlement rather than customer action, the timing mismatch behind most bridge-loan delinquencies is eliminated.

What does a real-time reimbursement estimation engine do?

It combines verified coverage data, extracted procedure codes, and historical insurer settlement data to produce a specific reimbursement-probability estimate before the financing decision is made. That lets the financing company underwrite against a confirmed expected reimbursement rather than an unverified claim.

What is the biggest technology gap in the US pet insurance financing ecosystem?

The absence of real-time insurer policy verification APIs that external financing providers can reach. Most carrier systems weren't built to expose this data externally. Until that changes through direct API development or document- and email-based automation as a bridge—financing companies are underwriting without the single most critical data point in their risk model.

What is the difference between pet insurance reimbursement and direct billing?

Under reimbursement, the owner pays the vet directly and files a claim to be repaid by the insurer. Under direct billing, the insurer pays the vet directly and the owner only covers their deductible or co-pay. US pet insurance is almost entirely reimbursement-based, which is the root cause of the financing gap.